A bond by any other name

Panda and dim sum bonds pave the road to an international RMB

International bond markets have some A+ branding. I say “international bond market” and you go zzzzzzzz. But I say “komodo bond” (a bond issued by a foreign entity in Indonesia) or “masala bond” (the same for India), and suddenly you have a powerful urge to apply to grad school for economics. China has two incredible ones: “panda bonds” for RMB-denominated bonds issued in China and “dim sum bonds” for RMB-denominated debt issued abroad or in Hong Kong or Macau. So good. And last month there was an intriguing first in China’s dim sum bond market. In mid-April, the Government of Portugal sold an eight-year, 1.99 billion yuan ($292 million) offshore RMB dim sum bond in Portuguese markets. A first for a euro-area sovereign.

Capital markets are vast and Byzantine, but the core idea is that they are the mechanism used to put capital to work. Instead of leaving a big pile of cash in a checking account, you buy bonds or equity from someone (who needs the debt to build a highway or data center or railroad), which earn more or less interest depending on risk. These markets are the beating heart of currency internationalization. For a bond to be RMB-denominated means the principal and interest will be paid back in Chinese renminbi (versus paid back in U.S. dollars for a dollar-denominated bond).

The offshore dollar system — eurodollars and dollar bonds issued outside the U.S. — created a vast, self-reinforcing ecosystem of dollar demand that exists outside of Washington’s direct oversight and control. China wants elements of that for the RMB — deeper offshore liquidity, broader adoption, and options for its currency — without sacrificing oversight. Beijing’s obsession with control is why the capital account (investment flows, rather than trade flows) stays mostly closed.

Dim sum bonds and RMB eurobonds help address the tension between control and expansion. They build global familiarity with the yuan among traders, investors, and eventually central banks, without compromising capital account control. Researchers at the Bank for International Settlements and Hong Kong Monetary Authority showed that offshore markets effectively let non-residents hold another country’s currency, taking on currency risk (the RMB goes up or down), while largely escaping country risk (Beijing suddenly imposing capital controls, freezing accounts, or changing the rules). The ability to divorce country risk from a currency makes that currency far more attractive globally.

Each new dim sum bond or RMB Eurobond deepens the RMB offshore market and each new panda bond deepens the appetite for access to Chinese capital. This is how reserve currencies are built.

Where bonds are being issued

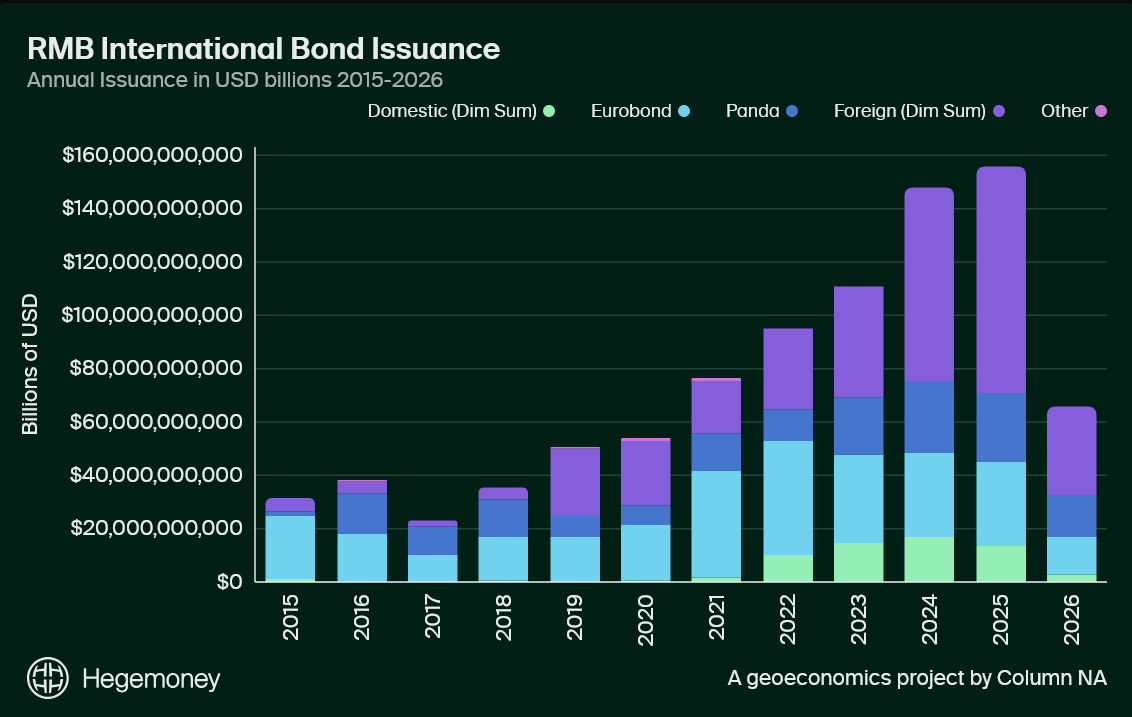

Since 2015, $885 billion in RMB-denominated international bonds has been issued in nearly 40,000 deals — running at a $195 billion annualized pace in 2026, on track to surpass last year. RMB-denominated bonds come in four distinct structures, each with different issuers and investors.

Much like dim sum, China’s international bonds come in many flavors (four main ones):

Pork. Haha. Just kidding.

Foreign dim sum bonds are issued in Hong Kong and Macau and make up the largest segment at $348 billion. Over 80% of the foreign dim sum bonds are issued by Chinese state issuers (more on this later).

Eurobonds are most attractive to Western institutional money that prefers familiar paperwork and clearing methods. Eurobonds are typically governed by English law, listed on the Luxembourg or London Stock Exchange, cleared through Euroclear/Clearstream, and generally exist outside China’s regulatory control. Despite totaling $299 billion across 37,230 deals, growth in issuance of Eurobonds has flatlined around $30ish billion annually since 2022, as they struggle to compete with the Hong Kong market’s deeper liquidity.

Domestic dim sum bonds are RMB paper sold by issuers in their home country (i.e. not China) with a total issuance of $62 billion over the last decade. This segment is worth watching because it builds demand for RMB paper outside of Hong Kong and China. The largest participant is Russia, whose exclusion from the dollar financial system has driven over $15 billion in issuance since 2022.

Panda bonds are debt issued by foreign entities inside mainland China, running at $172 billion over the last few years and growing — a sign that issuers see Chinese investors as important sources of capital. Of that $172 billion, probably around $50 billion was issued by truly foreign entities. The rest comes from Chinese and Hong Kong-parented companies incorporated offshore (largely Chinese property developers using Cayman Islands and BVI holding structures). We included these in the analysis to capture the largest possible size of the market. Yes, these are onshore while the rest of the market we’re talking about is offshore, but panda bonds are an important part of the RMB international bond ecosystem because they simultaneously open up China’s bond market and expand the scale of RMB-denominated financial assets in global markets.

Who are the issuers?

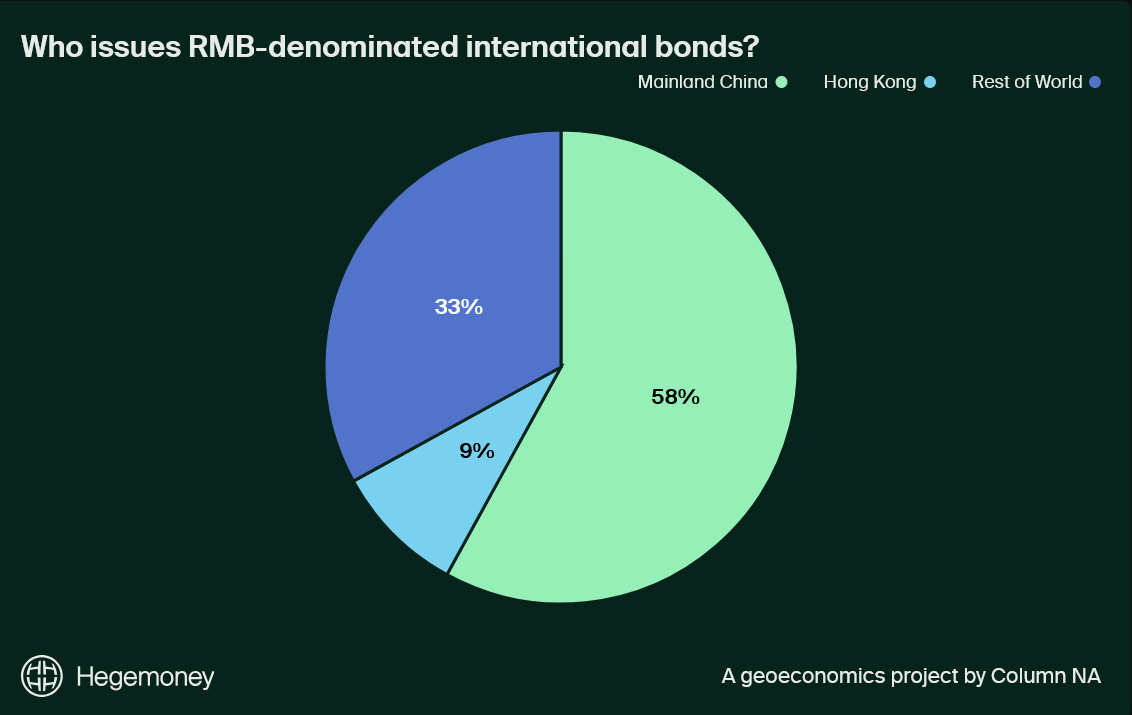

The breakdown of all RMB bond issuance is as follows:

58% from mainland Chinese entities

9% from Hong Kong

33% from the rest of the world

Let’s first discuss the Chinese entities’ motivations. The People’s Bank of China has issued over $200 billion in Hong Kong alone, with single deals now topping $8.8 billion. Yes, $200 billion is small peanuts in the capital markets game, but if you take a step back, Beijing is building the muscle to deepen its international capital market through a few mechanisms:

Benchmark yield curve. Offshore investors need a risk-free reference rate to price all other RMB assets against. By issuing offshore RMB bonds, Chinese state entities establish a benchmark yield curve and help other foreign issuers know what pricing is fair.

Depth. Chinese state entities are creating depth by ensuring high-quality assets for the growing pools of yuan accumulating in Hong Kong through trade settlement, keeping that currency circulating offshore rather than converting back into U.S. dollars.

Spread. Finally, issuing offshore debt allows the Chinese government to manage the spread between onshore (CNY) and offshore (CNH) yuan.

China does not want the RMB to replace the dollar. However, Beijing wants alternatives and will need a deep, liquid offshore RMB ecosystem before the currency can do all the government wants it to. Work by Menzie Chinn and Jeffrey Frankel confirms that the depth and liquidity of a currency’s primary financial center are among the strongest predictors of reserve-currency status. For the RMB, Hong Kong’s offshore market plays that role.

So which other countries are issuing bonds in RMB and why? We see three distinct groups and motivations.

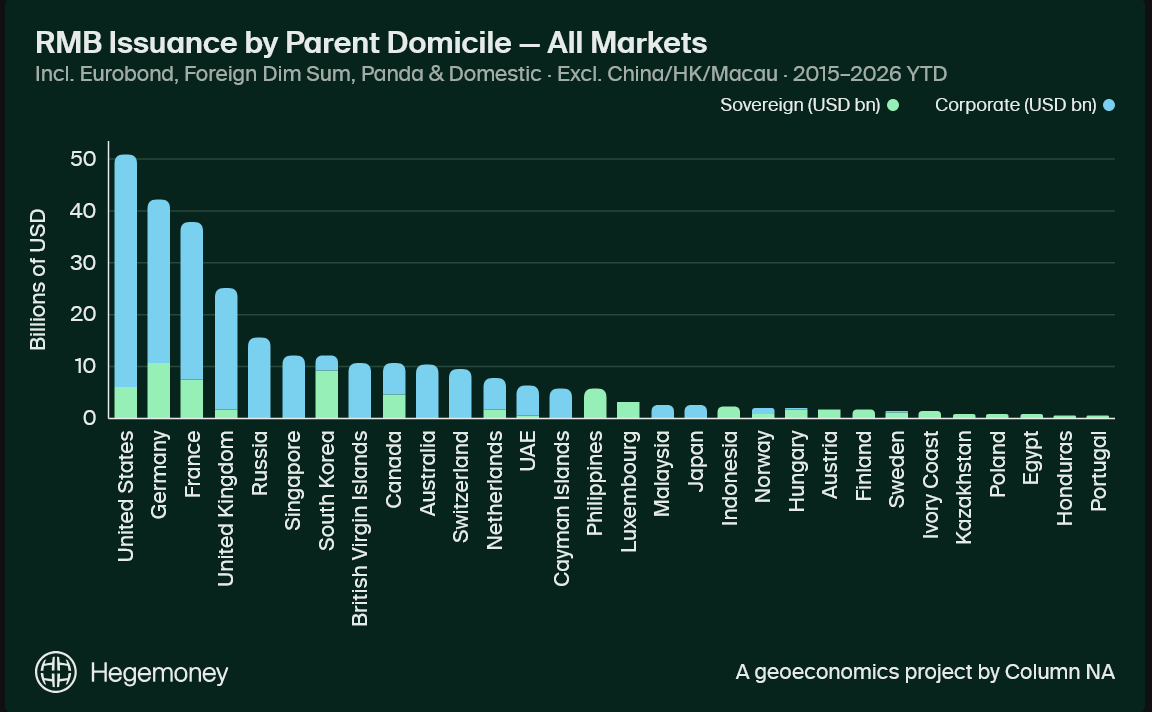

Note: the sovereign portion under the United States is not the U.S. Government issuing dim sum bonds but rather the multilateral institutions like the International Finance Corporation (headquartered in Washington, D.C.) issuing RMB-denominated debt.

Sovereigns. The smallest tier by volume is sovereign nations. The Philippines has issued RMB bonds twice. Poland, Egypt, and Slovenia all have sold paper in the panda market. Hungary is the most frequent flyer, issuing panda bonds six times since 2017, with the coupon falling from 4.85% to 2.5%. Chinese government bond yields have fallen steadily while U.S. rates surged. By 2023, the gap between U.S. 10-year Treasuries and Chinese 10-year government bonds had inverted to roughly 150–200 basis points — the largest such reversal in history — and has since widened further, with China’s 10-year bonds currently yielding around 1.75% against U.S. Treasuries above 4%. For a sovereign borrower that holds reserves in dollars but spends in local currency, locking in RMB funding at sub-2% rates while the dollar alternative sits above 4% represents shrewd accounting more than a geopolitical statement.

Portugal has now come to the RMB bond market twice, in two different categories. These deals are rarely above $500 million, but are important for two reasons. First, with panda bonds, it shows that countries like Portugal recognize the Chinese market is important for growth, and generally investors (prospective Chinese investors!) want to hold investments in their own currencies. And for Portugal’s domestic dim sum, they are building a constituency in Portugal for continued RMB engagement — which presumably signals a growing financial and economic entanglement between the two countries.

Wall Street and the City. U.S.-parented corporate entities account for $45 billion — the largest single non-Chinese bloc. This is mostly the U.S. financial sector: Goldman Sachs, Citigroup, Merrill Lynch, JPMorgan, and Morgan Stanley issuing RMB debt through their European and Hong Kong entities, tapping two pools of RMB demand simultaneously. UK-parented entities add another $25.3 billion. These are largely financial intermediaries using RMB as a funding currency for their Asia operations, not ideological converts to yuan finance.

German industry. Germany is the largest non-Chinese user of the panda bond market by a significant margin — $25 billion in panda bonds when measured by parent domicile. Mercedes-Benz has issued panda bonds every single year since 2015. Volkswagen, BASF, and Bayer followed. Mercedes-Benz issues panda bonds because China is an incredibly important export market and the company wants its debt in the same currency as its revenues. This is a durable form of RMB adoption because it is entirely apolitical, driven purely by the economic heft of China and the importance of the Chinese consumer to foreign demand. Other corporations are showing up here as well. Again, and in addition to operational hedging purposes, the yield differential is powerful: if you can raise debt 200bps lower in RMB, what business wouldn’t make that decision? It’s also interesting that KFW, the German development bank, has been a large user of the RMB Eurobond market to the tune of $9.7 billion.

Step by step

$885 billion of RMB International bond issuance sounds significant until you remember that 58% of that volume is China selling to itself and the rest is mostly Wall Street doing treasury operations. Genuine foreign adoption is a much smaller number, and wow does it pale in comparison to USD liquidity. But panda and dim sum bonds grow every year, and the cost of entry to new issuers falls every year, both of which are small increments in China’s favor.

For all the furor over the petrodollar and petroyuan in recent weeks, it’s important to keep our eye on the ostensibly boring but wonderfully branded structural stuff happening elsewhere!1

I learned a lot from yet another of your excellent articles. I have no idea why it has affected me this way, but I am left shaken, not stirred. 😉 Keep up the great work.