Diagnosing dollar dominance

USD is much more than a reserve currency

We know what has made the dollar dominant — economic size, deep capital markets, institutional credibility, geopolitical reach, network effects. These pillars are well understood. But we don’t pay enough attention to how we measure dominance.

The conversation around dollar dominance normally defaults to reserves. Central banks around the world have cut U.S. dollar reserves from 70% of total foreign exchange (FX) reserves in 2000 to 57% in 2025, and pundits read this as terminal decline. But reserves are only one of three distinct roles the dollar plays and arguably the least diagnostic:

The dollar is the world’s vehicle currency.

The dollar is the world’s funding currency.

And, despite some erosion, the dollar is still the world’s dominant reserve currency.

Gopinath and Stein showed that the vehicle and funding currency roles form a self-reinforcing loop: trade invoiced in dollars creates global demand for safe dollar assets, which lowers the cost of borrowing dollars. Exporters then invoice in dollars to match their dollar liabilities with dollar revenues, and the cycle reinforces itself. Reserves correlate strongly with these other roles — central banks tend to hold the currency their economies invoice and borrow in — but the causation runs through trade and finance, not the other way.

Erosion in one role doesn’t automatically cascade into catastrophic failure in the others, but it can destabilize the dollar ecosystem. To diagnose dollar dominance honestly, we have to watch all three.

Vehicle currency: the dollar remains durable

When two countries love each other very much... Ahem. Sorry. When two countries engage in trade or some sort of cross-border transaction, they have to decide what currency they’re going to use in the transaction. Is someone handing over a fistful of euros? A suitcase of yuan? A troy ounce of gold dust (God forbid)? No, more likely than not, dollars will change hands.

The dollar is the world’s vehicle currency in two complementary senses. First, in trade, it’s the currency that exporters and importers invoice in, even when neither is American — this is known as the dominant currency paradigm. Second, in FX markets, it’s the bridge currency that connects all other currency pairs. It’s cheaper to go from Korean won to USD to Brazilian real than directly from won to real. This is another example of a dollar-reinforcing cycle: trade invoiced in dollars generates dollar FX activity, and a dollar-centric FX market makes dollar invoicing cheaper through tighter spreads.

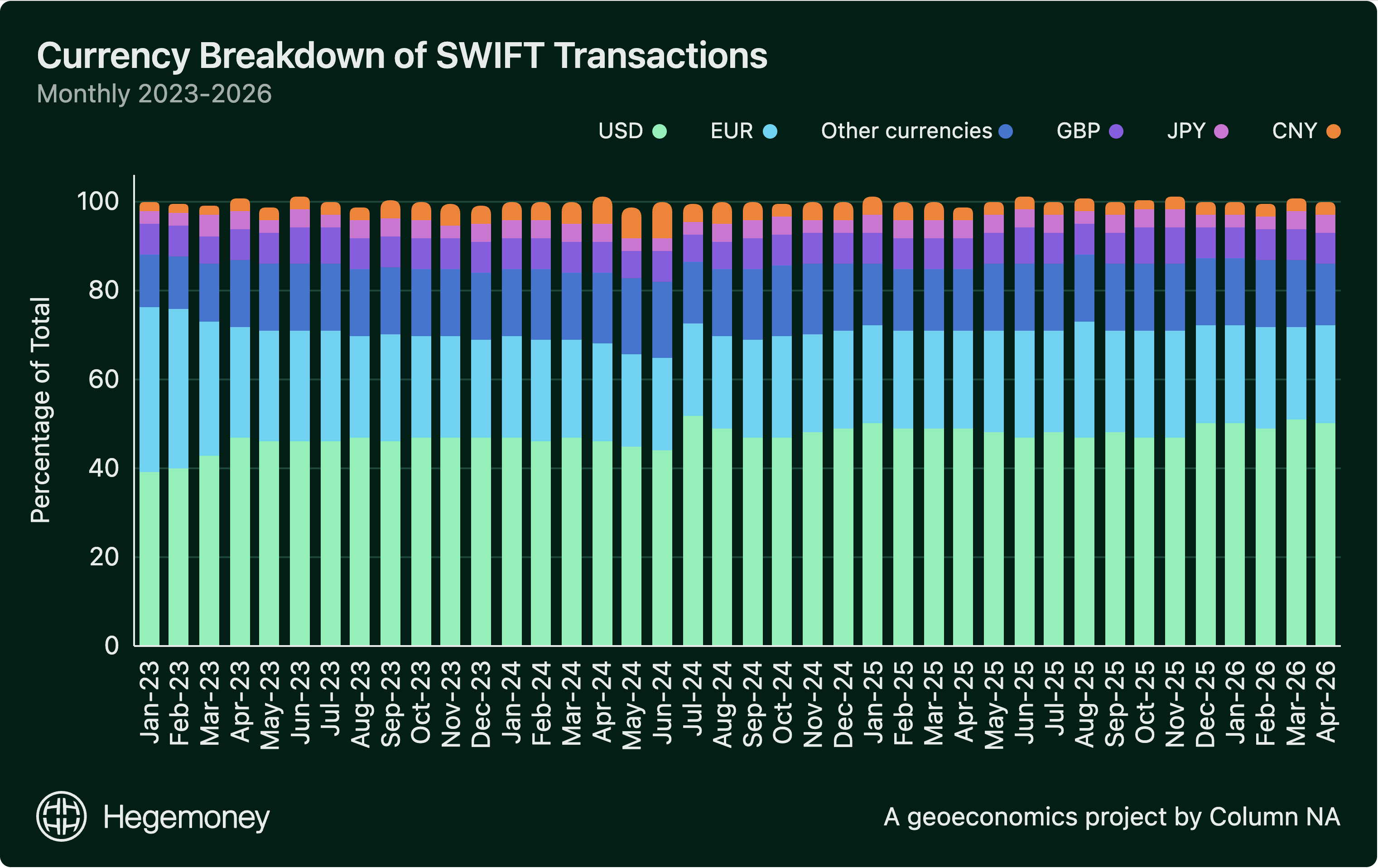

I would argue that this is the most durable measure of dominance. According to the BIS Triennial Survey, 89% of all foreign exchange transactions still involve a dollar on one side. The SWIFT data tells a similar story: USD’s share of cross-border messaging traffic has held steady around 48–50% for the past three years. According to IMF research, a large share of USD payments occur between third-country originators and beneficiaries — meaning the U.S. is involved on neither end of the transaction — the textbook sign of a vehicle currency.

This data is notoriously difficult to aggregate, and we must rely on proxies such as the SWIFT data to estimate currency composition of trade invoicing. A group of IMF economists hand-assembled a 132-country panel, which is likely the most robust data set available, and they noted that the dollar accounts for an average of 49% of export invoicing, several times the U.S.’s actual share of world trade. The available proxies are also missing some flows such as those between Russia and China in RMB, non-SWIFT transactions on China’s CIPS system, book-to-book transfers, and crypto. But for now, those transactions are still small in the scheme of global payments. SWIFT, on average, sent 51 million messages a day in 2025, while CIPS averaged around 36,000 daily transactions.

What explains the dollar’s durability as a vehicle currency? Network effects. Krugman showed in 1979 that vehicle currency status is self-reinforcing: the more a currency intermediates transactions, the deeper its markets, the lower its transaction costs, the greater its appeal. Displacing a dominant vehicle currency requires a degree of volume that no other currency can muster. However, new payment systems (CIPS), their linkages (fast payment bilateral connections), and new technologies (CBDCs) all have the potential to shrink transaction costs and lower barriers to entry to transaction intermediation for other currencies, so beyond just volume we have to keep an eye on what other countries are building.

Funding currency: sticky, but rate-sensitive

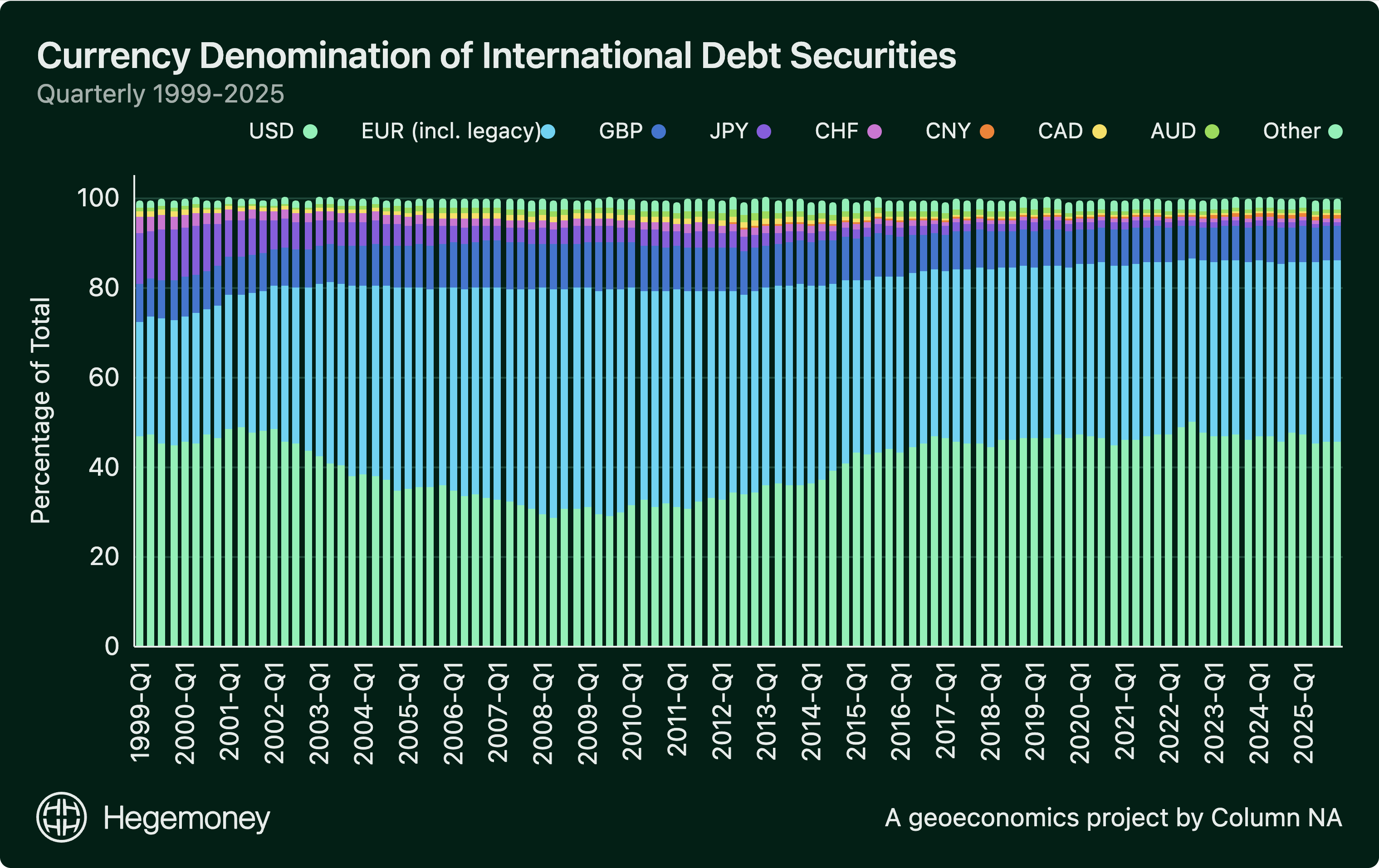

A funding currency is what the world borrows in. Ghana issues bonds in dollars because global investors don’t feel great about holding cedi. A Brazilian firm borrows dollars at rates a reais-equivalent bond can’t match. A multinational raises dollar debt to match dollar-denominated revenues from global operations.

The BIS data shows USD at 45.7% of international debt securities outstanding in 2025-Q4. EUR sits at 40%, GBP at 7.5%, RMB under 1%. These shares have barely moved in a decade. Even with sanctions, BRICS rhetoric, and explicit de-dollarization policy, the composition of international debt has not shifted. Everyone borrows in dollars because, well, because everyone else borrows in dollars — which creates deep and liquid markets, which makes it cheap to borrow in dollars, which reinforces the cycle. Breaking that equilibrium would require a credible alternative, and no other currency comes close.

But funding is the most rate-sensitive of the three roles. When dollar rates stay elevated, the cost advantage over other currencies narrows. Mozambique is reportedly in talks to convert dollar debt to RMB at a likely 200bp discount. With the U.S. 10-year note nearing 5%, more emerging-market borrowers eye debt conversion to keep their debt servicing costs low.

Reserve currency: geopolitical troubles

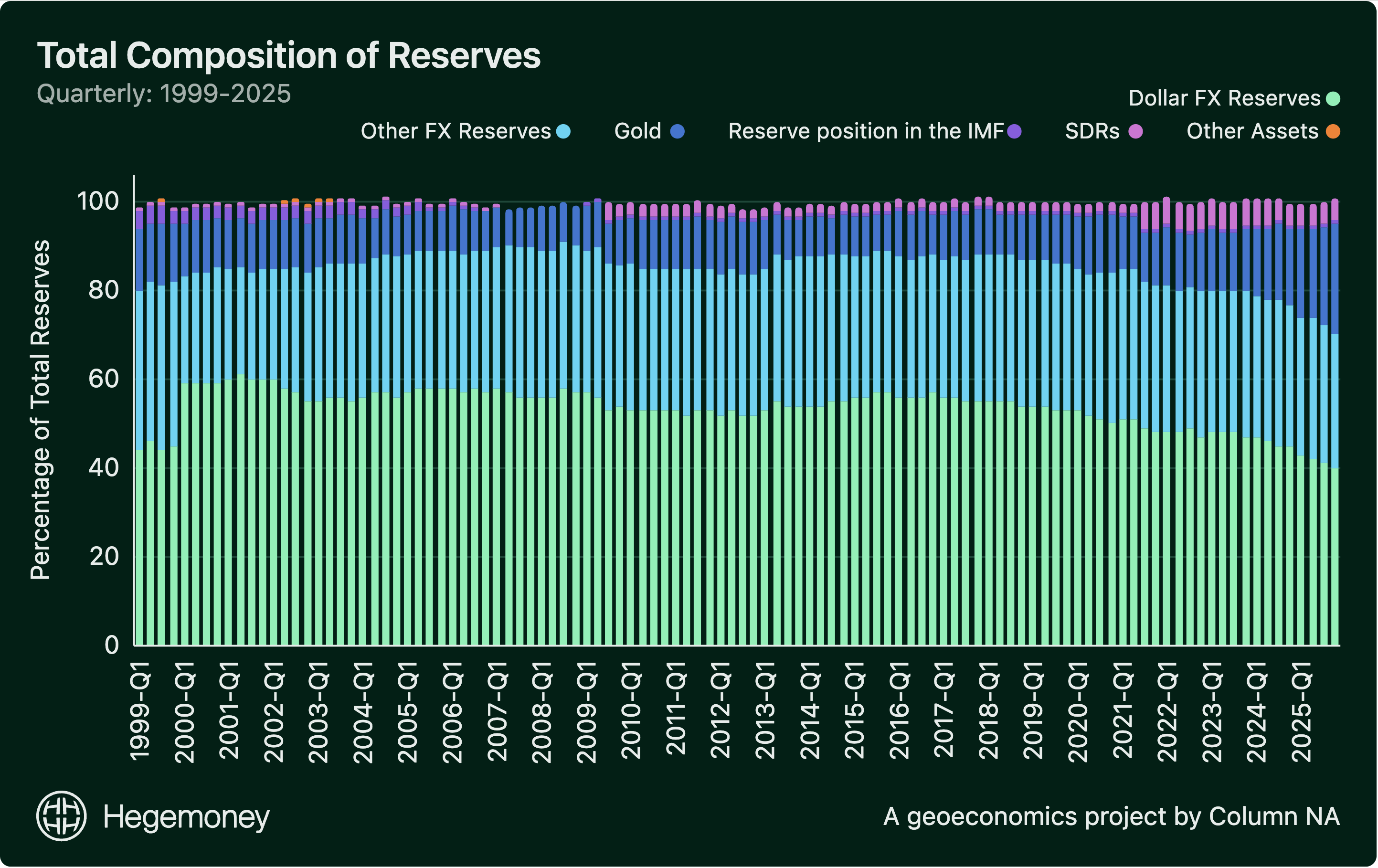

This is where the conversation usually starts and ends. Central banks have cut dollar reserves from ~60% of total reserves (all assets) in 2000 to ~40% in 2024. Okay. That is a meaningful erosion, I admit, but what replaced those dollars?

Mostly gold. Gold now accounts for roughly 25% of global central bank reserves, up from under 10% two decades ago, with central bank gold demand hitting record highs in 2025. It is not controversial to say that the freezing of Russia’s dollar reserves in 2022 accelerated the shift toward gold, and now even non-sanctioned countries hedge against the dollar (or more accurately, hedge against exposure to the U.S. government’s conditions for holding dollars).

But gold can’t invoice a trade, fund a bond, or clear a payment. It’s a geopolitical hedge, not a rival currency. A Korean exporter still settles in dollars regardless of whether Brazil’s central bank holds gold or dollars. If central banks were shifting from dollars to euros or renminbi — that is, to other transacting currencies — that would be more concerning. Reserve accumulation is generally a reflection of what currencies a country’s central bank collects when their exporters trade. A shift from dollars in reserves to other fiat currencies might suggest that the dollar is being used less in trade invoicing.

So yes, the data show that the share of reserves is eroding, but in a way that doesn’t meaningfully threaten the primacy of the dollar’s other two roles yet. Keep in mind that Eichengreen, drawing on historical precedent, reminds us that reserve currency transitions are notoriously slow. The pound sterling did not vanish from reserves when Britain’s political hegemony declined in the twentieth century; it took generations to erode. However, it’s far too soon and hazy to say with any confidence that dollar reserves are irreversibly eroding in a similar fashion.

I’ll let you know when my local dive lets me buy a round of Miller High Life in gold.1

A wonderful exposition.

It took 30 years 1915 to 1945 for GBP to USD - people forget this, yes.

The US-CN 10Y differential will drive trade financing especially in the Global South. Everyone trades with China and 300 bppa is not to be sneezed at.

Really great outline of foreign currency transactions and why central banks holding more gold doesn't necessarily mean USD dominance is going to decline. Found it interesting the point about the GBP taking decades to decline even after UK political/military dominance eroded more quickly.