Dollars and strikes

An examination of the dollar following U.S. military strikes

Within 72 hours of the first strikes on Iran, six U.S. service members were dead, Dubai International Airport was closed, oil had spiked higher, the Middle East was in open regional war — and the dollar was up over 1.5%.

The obvious explanation here is that the dollar is the world’s ultimate safe haven asset, and USD rises when geopolitical risk spikes.

However, this hasn’t been the case historically.

History shows short-term weakness or a muted reaction after strikes

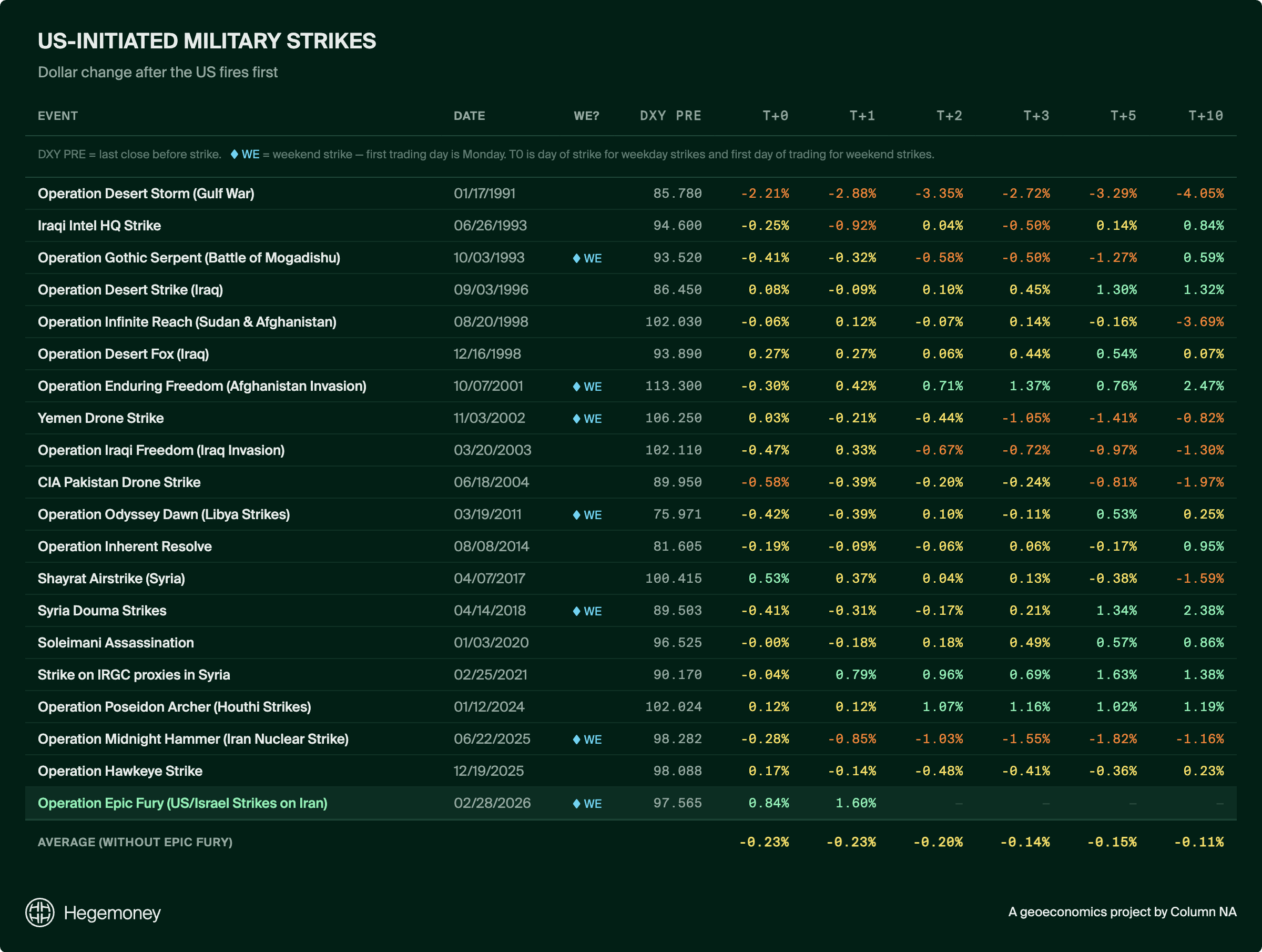

After the dollar surged on Monday, I wanted to see if this was a consistent pattern following kinetic U.S. engagement, so I looked at the behavior of the dollar index (DXY) immediately after U.S.-initiated strikes going back to 1991 — 19 events in total, from Desert Storm to the Syria strikes to the Soleimani assassination (see footnote for an explanation of the methodology for selecting these strikes)1. The pattern is counter-intuitive for a safe-haven asset. Instead of roaring higher in a universal risk-off trade, in the immediate days (1–3 days) after the strike the dollar was either down or relatively flat (moving less than 0.5%). On average, the dollar index moved -0.23% on the first trading day following the attack, and -0.15% a week after the first strike.

The data suggests that historically the dollar does not see a surge in safe-haven demand in the immediate aftermath of a U.S.-initiated strike.

Why does the dollar typically fall right after a strike?

The short-run mechanism isn’t complicated once you unpack it. U.S.-initiated military action in the Middle East can easily become an inflationary event. Oil prices rise on supply disruption fears (less oil = more expensive oil) and shipping costs spike (very costly and long detour to avoid the Strait of Hormuz). The cost of shipping oil from the Middle East to China just hit an all-time high, increasing almost 100% by Monday as some insurance companies canceled war risk coverage. That makes energy more expensive. Higher oil prices act like a tax on households and businesses, weighing on growth, stoking inflation, and putting the Fed in a difficult position as they balance controlling higher prices against cushioning growth. That combination has historically put downward pressure on the dollar, even when American oil companies are benefiting. Markets are forward-looking, so just the anticipation of this disruption and subsequent inflationary pressure can create more dollar sellers.

The market may also start to price in a longer-term conflict. The academic literature is clear about what happens to currencies over the arc of a war. To fight wars, governments spend money. That spending gets financed through debt. Although previously the US had raised taxes and cut spending to pay for wars, the post 9/11 playbook moved us into the era of debt-financed conflict. More debt means more issuance of U.S. Treasuries, which means more dollars in circulation — another structurally inflationary factor. A study by Christopher Warburton found that the dollar depreciated at an average monthly rate of 1.2% during the Iraq War.

Are the Iran strikes different?

And yet, this week we saw oil and the USD surging higher together. A few thoughts on why this time could be different:

The short squeeze. Before the first bomb dropped, the dollar was already down 9% over the past year. According to Bank of America’s fund manager survey, shorts against the dollar reached their highest level since 2012. When that many people are leaning the same way, it only takes one unexpected catalyst to trigger a cascade of forced covering. The death of Khamenei could have fueled a panic closing of crowded shorts that contributed to the stronger dollar.

Market dysfunction. Okay, hear me out. This is the first time the Strait of Hormuz, which transports one-fifth of the world’s oil, has effectively closed and this has likely jammed the plumbing of the financing of the global oil trade. Trading firms with derivative positions suddenly need dollars to cover margin calls on positions moving sharply. At the same time, letters of credit used to finance the frozen shipments tie up dollars on banks’ balance sheets, effectively locking them until the trade can be resolved. Buyers also need replacement oil, which requires new letters of credit and additional dollar commitments. Multiply that across a lot of tankers and you get a sudden scramble for dollars.

Macroeconomics. The macro backdrop today is the opposite of almost every previous strike episode in the dataset. During the majority of these military campaigns, the Federal Reserve was actively cutting rates or sitting near cycle lows. This time, the Fed has paused its monetary easing and some officials are considering if it is time to resume tightening. One of the few times that saw dollar strength following a strike was after Operation Poseidon Archer (2024–2025) and this coincided with the Fed Funds Rate at its cycle peak. The implication is that when rates are expected to be higher in the U.S. (i.e. tightening cycles) compared to similar securities, money will chase the higher yield regardless of what is happening with the military.

Structural geopolitical bid. Academic research argues that international reserve currency choice is driven not only by economic factors like market size, capital markets, and credibility, but also by geopolitical ones. Barry Eichengreen has noted that military alliances can boost a currency’s share in a partner’s foreign reserves by roughly 30 percentage points. As we face the potential of prolonged conflict, one could argue that dollar asset demand from our allies is lending support to the USD.

The scale of potential change. History doesn’t help us here. Iran has been the central organizing adversary in Middle Eastern geopolitics since 1979 —shipping weapons to the Houthis, supporting proxy militias in Iraq, arming Hezbollah in Lebanon, and funding Hamas in Gaza. For nearly half a century, every risk premium embedded in oil markets and every concern over nuclear proliferation bore the fingerprints of the Islamic Republic. Markets may be looking past the immediate chaos and asking genuinely new questions: what does the world look like without this Iranian regime and what will the next iteration look like? Those questions are balanced against an older and weightier fear: could this be the start of a worldwide conflict?

History strikes back

I’ve focused only on immediate price action — the first 72 hours of a conflict with Iran that could last months or years. The rise in the dollar is supported by technical, structural, and macro factors, and those may be enough for continued support. If the dollar falls over the next few weeks, it doesn’t mean it is no longer a safe haven. Maybe the conflict is subsiding or maybe history is just reasserting itself.2