Imbalances build war chests

And are growing much harder to fix

Global imbalances — the large and persistent current account surpluses and deficits that have defined the world economy for decades — can be dangerous for global stability. We’ve known this for years. So why do we tolerate them? Why can’t we fix them?

First, there’s active disagreement on what causes deficits, with two schools of thought each prescribing different policy responses and muddying our response.

Second, solving imbalances requires either painful domestic policies that governments won’t implement voluntarily, or coercive international instruments outside the norms of the rules-based order.

Third, the framework under which the rules-based order governed previous conflicts on imbalances is kaput. With the return of great power competition, rising conflict, and weaponized interdependence, countries will view surpluses as a way to build war chests — and what country in their right mind is going to willingly sacrifice that.

A primer on the balance of payments (skip if sufficiently nerdy)

The balance of payments consists of all transactions between a country and the rest of the world. It is divided into the:

Current account

Capital account

Financial account

It is an accounting identity, so in theory, the whole thing sums to zero.

The current account captures flows of goods, services, and income. It consists of three main parts: the trade balance (exports of goods and services minus imports), the primary income balance (net earnings from abroad such as dividends, interest, and profits), and the secondary income balance (current transfers such as remittances and foreign aid).

A current account deficit occurs when a country spends more on imports and payments to foreigners than it earns from exports and income received from abroad.

The capital account covers one-off transfers like debt forgiveness, and deals involving things like patents or brand names. It is usually small.

The financial account includes foreign direct investment (when a company builds a factory or buys a business abroad), purchases of stocks and bonds, bank loans and deposits, and changes in the central bank’s official reserves (such as foreign currency and gold).

I don’t care who broke it. Someone fix it!

Economists have been debating the merits, risks, and underlying causes of trade imbalances since at least 1628, when the English merchant Thomas Mun argued that a nation’s wealth was built by exporting more than it imported and accumulating the difference in gold.

And after centuries of debate, two schools have emerged:

The orthodox school

This is the position that dominates the IMF, most central banks, and the bulk of academic economics. It holds that current account imbalances are the result of domestic savings and investment decisions. A country that saves more than it invests runs a surplus. A country that invests more than it saves runs a deficit. The orthodox school holds that current account imbalances are fundamentally driven by domestic policy choices (fiscal, monetary, structural, and regulatory).

For example, Chinese domestic policy disincentivizes spending while American domestic policy does not. Maurice Obstfeld points out that dollar dominance plays no role in forcing deficits because 1.) history has shown that the United Kingdom had reserve currencies and current account surpluses, and 2.) dollar demand can come from the offshore dollar market, not just through trade.

The heterodox school

The heterodox school disagrees on what causes current account imbalances. It posits that large autonomous capital flows — e.g. reserve accumulation by central banks in countries running a surplus, flight-to-safety dynamics, global demand for dollar-denominated safe assets — are the primary driver. The heterodox school assesses that the financial account determines the current account, and therefore the dollar’s reserve currency status creates a permanent bid under the dollar that makes U.S. exports persistently uncompetitive regardless of what Washington does with its budget.

The two schools both agree that distortive domestic policies — suppressed consumption, fiscal deficits, managed exchange rates — shape a country's own current account balance. Where they split is on how far those distortions travel. Maurice Obstfeld and the orthodox camp hold that exchange rates are not a sufficient statistic for the trade balance but acknowledged that demand for the dollar due to its reserve status may make the dollar stronger against foreign currencies than it would be otherwise. In a recent article, Brad Setser and Shahin Vallée counter that China's currency undervaluation is a first-order force driving its ballooning surplus and the global imbalances that follow.

Even though the two schools can’t agree on why we have imbalances, they largely do agree that imbalances are dangerous in two distinct ways:

Financial fragility: Persistent deficits eventually become large net liability positions internationally (you owe other countries a lot of money). When investors begin to question the economic dynamics of a country running big deficits, capital flows can reverse, creating large outflows that cause sharp currency adjustments and an inability to fund government spending. As the provider of the world’s reserve currency, the U.S. is at less of a risk of severe capital flight, though the world is highly exposed to U.S. assets which would increase potentially catastrophic ripple effects of a financial crisis that originated in U.S. securities.

Beggar-thy-neighbor: Protective measures that increase export competitiveness — through labor laws or currency management — can have negative impacts on trading partners. A paper from several years ago showed that the 2000-2012 trade shock from China reduced manufacturing employment as a share of the American working-age population by about 1.6 percentage points from 2001-2019. The IMF notes that perceptions of unfair trade practices can fuel protectionist policies that undermine global commerce.

Again, both schools of thought largely agree that imbalances are dangerous and the current trajectory is unsustainable. And yet forty years of combined intellectual effort have led us to large and persistent global imbalances.

Have we learned nothing from history?

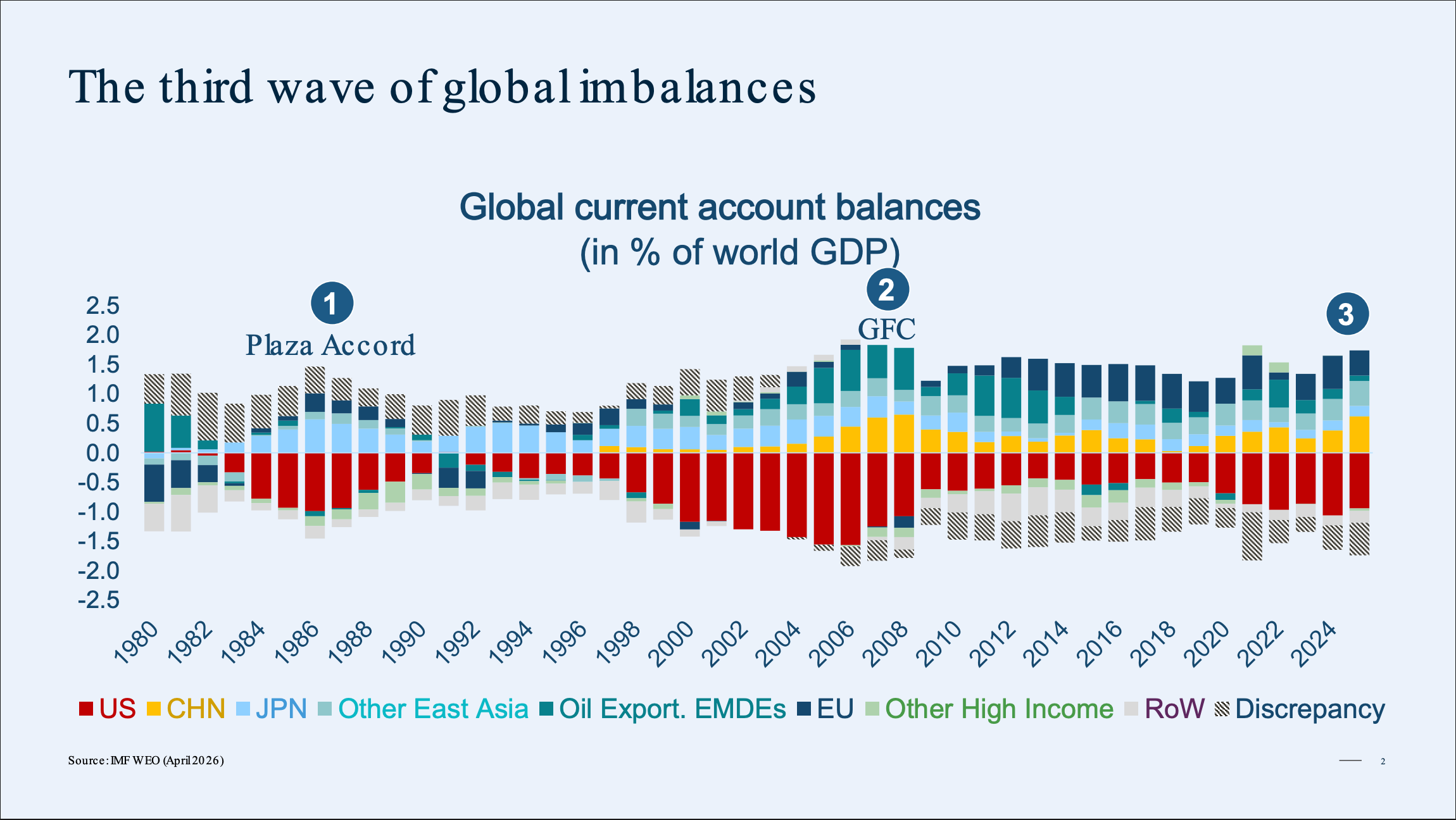

Gita Gopinath of Harvard identifies three waves of global imbalances characterized by persistent U.S. current account deficits in the post-Bretton Woods era.

The 1980s: The Plaza Accord of 1985 marked the first coordinated attempt to address global imbalances, with G5 finance ministers agreeing to weaken the dollar. Congressional threats of protectionist legislation gave surplus countries strong incentive to cooperate. The Accord depreciated the dollar and defused the immediate protectionist threat, and imbalances did eventually narrow — though only after a two-year lag as domestic fiscal adjustment and a slowdown took hold. However, the underlying export-led growth model remained intact for many rising economies.

The 2000s: After the Asian Financial Crisis, dollar reserve accumulation surged as countries sought insurance against future shocks. The resulting “global savings glut” (per Bernanke) pushed capital into U.S. markets and the American deficit widened alongside it. U.S. policymakers debated the causes of these inflows, but the Global Financial Crisis interrupted the debate and temporarily accomplished what policymakers couldn’t do on their own: a reduction of imbalances.

Today: The net global imbalance has returned with a vengeance. China’s trade surplus has reached record levels while the U.S. current account (the trade balance plus the income America earns on its overseas investments) keeps deteriorating.

So we’ve learned that it takes either a coordinated currency intervention coupled with painful domestic adjustments or a global crisis to temporarily relieve global imbalances. Which doesn’t exactly arm us with many sophisticated policy options. This gives “We had forty years of global imbalances and all I got was this lousy t-shirt” vibes.

The game has changed

Policymakers have long shared the assumption that countries running surpluses would eventually respond to economic pressure because those surpluses were economic instruments with economic aims. That is no longer the case.

China’s domestic financial repression and forced saving are how Beijing accumulates buffers against external shocks, builds industrial capacity, and maintains the export dominance that both creates chokepoints (e.g. access to critical minerals) and buys political relationships across the developing world. We are kidding ourselves if we think that asking China to dismantle a strategic instrument in exchange for incremental macroeconomic welfare gains that accrue to Chinese households rather than to the Party will fall on anything except deaf ears. Why would any country give up a war chest after idealistic multilateralism has given way to pragmatic transactionalism?

After Crimea, Russia spent eight years deliberately accumulating reserves and running current account surpluses, explicitly to insulate the economy against external shocks. Russia invaded Ukraine with $643 billion in reserves that it probably planned on using to fund the war. Then the West froze those reserves in one of the most consequential actions of geoeconomic policy in the last century.

Surpluses buy buffers; buffers enable geopolitical risk-taking; risk-taking triggers sanctions; sanctions prove you needed bigger buffers. Then the cycle continues.

Deficits, too, can be part of a statecraft apparatus. For the United States, the dollar’s reserve status supports deficit spending, which can be used to fund initiatives (including, right now, a war with Iran).

Release the Karen

You can make an agreement with your neighbor on how to share common spaces. You cannot tell them how to clean their home. But when your neighbor’s neglected plumbing issue floods your basement, the president of the homeowners association gets involved and things get ugly. It is time for the G7 to start acting like the world’s most terrifying homeowners association.

New frameworks from the G7 and IMF are the most serious update to the orthodox playbook in years. The big goals are directionally correct: U.S. fiscal consolidation, Chinese consumption-led rebalancing, and European capital market integration. The institutional proposals in the G7 framework — WTO safeguard reform to cover sectors rather than individual products, expanding WTO trade rules to include trade-adjacent policies like cheap credit and land, and reinterpreting existing WTO laws to provide better trade protection for the purposes of national security — are useful. But both frameworks are reactive, not proactive, and are still asking countries to voluntarily dismantle strategic instruments in exchange for diffuse welfare gains for the commons. No one has bitten on that particular bait in forty years.

The heterodox toolkit is more honest about the need for coercion. Proposals like taxing capital flows, unilateral currency intervention, and price-based disincentives on capital account flows make it much more painful to run a surplus. Pain often works better than asking nicely. A 2019 bill in the U.S. Senate proposed imposing a market access charge on foreign capital inflows administered by the Federal Reserve under a current account balance mandate — the logic being that recycling your surplus into our markets should carry a price.

There is a pragmatic middle ground that combines both approaches. We should target domestic policies everywhere that suppress demand, deliberately suppress exchange rates, fail to support investment, encourage excess spending, distort factor prices, or spill imbalances outward. Michael Pettis points to China’s hukou system as a prime example: by restricting migrants’ urban rights and suppressing wages, it functions as a de facto trade intervention in China’s favor. The only lever we have to fix these imbalances is cost; Countries that can’t get their houses in order should face escalating penalties including restricted market access, capital flow surcharges, financial infrastructure restrictions, calibrated to measurable progress against the underlying domestic policies driving the spillover. Admittedly, restricting access to international markets as a penalty for domestic policies is controversial. But we’re in uncharted territory here.

One of the greatest lessons of the Plaza Accord is that it got countries to act because Congress made the threat of shutting off access to U.S. markets credible enough that Japan agreed to play ball. Credible threat forces cooperation, but threats are only credible when consistently followed-through when countries shirk their commitments. No country surrenders a war chest voluntarily. But countries do respond to incentives. 40 years on, we are still having the same conversation on global imbalances. To make the global economy more resilient and protect the stability of interdependence, we need to act on imbalances and, frankly, it's time for the homeowners association to get involved.1

The most interesting shift here is that imbalances are no longer just economic distortions — they are becoming instruments of statecraft.

If surpluses function as war chests, industrial-policy tools, and buffers against sanctions, then voluntary rebalancing is much harder to imagine. What looks inefficient from a welfare perspective can still look rational from a geopolitical perspective.

The core loop seems to be: surpluses buy buffers, buffers enable risk-taking, risk-taking triggers sanctions, sanctions prove you needed bigger buffers.

Same with domestic imbalances - the national debt.

Gold made rebalancing automatic.

Fiat makes rebalancing political.

The orthodox error is to use commodity-standard economic theory in a fiat world.

The heterodox error is to treat fiat discretion as liberation, while underpricing the politics that discretion creates.

We have to wait on politicians to correct imbalances and they won’t until they have to or until it’s too late.