Over the moon

SpaceX represents the best of American equity dominance

Last week, the world witnessed the largest IPO in history. SpaceX debuted on the Nasdaq, raising $85.7 billion and pushing past $2 trillion in market value after its first day of trading. Not only did this make Elon Musk the world’s first trillionaire (you go, Glen Coco), but the IPO also served as a vivid reminder of America’s equity dominance: the ability to convert new technology into financial assets and to wield access to those markets as a source of geopolitical leverage.

Built to absorb it

At the insistence of my editor that I not wade into the business of personal investment advice Substacking, I won’t comment on whether a company that had a net loss of $5B in 2025 deserves to trade at a $2 trillion valuation or is capable of reaching trillions in revenue within 15 years. Not my lane. In fact it doesn’t matter what you think about the fundamentals of the stock.

What are much more remarkable are the fundamentals of the U.S. market. The fact that American financial markets easily absorbed a $2T listing — and the fact that listing had two exchanges to choose from! — is nothing short of extraordinary. The U.S. once again proves it has the deepest and most liquid capital markets in the world.

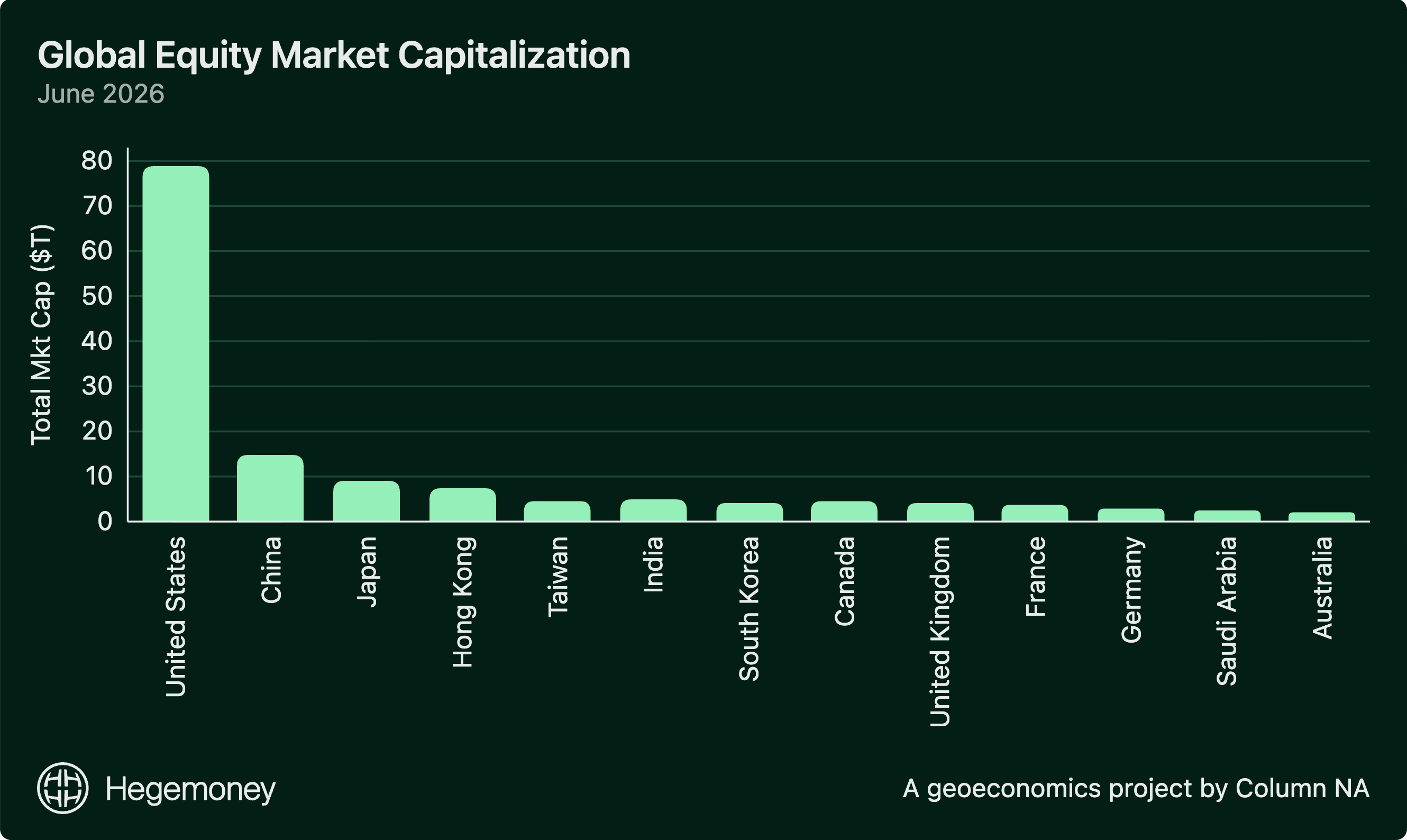

SpaceX increased U.S. equity market capitalization to $78 trillion. The next biggest equity market is China with $15 trillion, followed by Japan with $9 trillion. America’s equity market is larger than the rest of the top 10 largest national markets put together. A $2 trillion listing is large but comfortably absorbed by the U.S. market. In every other major market, it would represent an outsized portion of the entire national stock market.

SpaceX represents around 2.5% of U.S. market cap, but had it been listed on a Chinese or a Hong Kong exchange it would have represented 15% or 30% of market cap, respectively. It is hard to find comparisons. Saudi Aramco, whose IPO was large in absolute terms, was listed on the Saudi Exchange, Tadawul, where the company accounts for roughly 67% of total market capitalization — with only a tiny public float of 1.5–2.5% actually available for trading. Not exactly a broad and liquid private-sector listing.

The sheer size of the capital raised ($85B) would also have strained other exchanges. The previous record, Saudi Aramco’s 2019 listing, raised $25–29 billion. Even Hong Kong, which was the strongest IPO venue in 2025, raised $37.4 billion across all listings, roughly half of SpaceX’s single-day raise. This extraordinary depth of institutional capital, venture funding, retail participation, and secondary market liquidity gives the United States unmatched ability to price and fund frontier technologies at scales that no other nation can match. It is a foundational pillar of American equity power.

Light the fuse

SpaceX was incubated by a unique public partnership: NASA’s Commercial Orbital Transportation Services (COTS) program was the agency’s pioneering effort, launched in 2006, to pair limited seed funding with an anchor-customer commitment and fixed-price milestones. Private firms like SpaceX bore the development risk and cost overruns, while keeping their intellectual property and having the runway to build commercial markets for predictable government demand. We’ve seen a spectacular result in SpaceX’s pioneering of reusability and high launch cadence, collapsing launch costs and saving billions in taxpayer money.

No country has implemented this model for space companies at comparable scale or achieved comparable commercial outcomes. In Europe, the European Space Agency relies on the “juste retour” principle (allocating work based on member-state contributions). A 2023 Bruegel paper and the 2024 Draghi report on European competitiveness note that this approach leads to political compromises, inefficiencies, and slower progress on cost and reusability. In China, even “private” space firms operate under military-civil fusion policies that subordinate commercial priorities to state and military goals.

COTS shows how governments can catalyze private-sector innovation by structuring demand in a way that shifts risk to private firms while rewarding performance. Obviously SpaceX has since expanded beyond just rockets into satellites and AI, which greatly drove the valuation, but COTS gave the company the initial boost it needed to become one of the world’s most valuable enterprises.

Not invited to PLA(y)

Foreign firms list on U.S. exchanges primarily to access deeper capital markets at a lower cost of capital, increase liquidity, broaden their shareholder base, and gain prestige. U.S. markets also generally offer higher valuations for companies because investors have greater confidence in shareholder protections, disclosure standards, and market liquidity. Over the last 20 years the P/E ratio of the S&P 500 has on average been 18% higher than that of its international counterparts. American markets also attract the most foreign capital — not by percentage (the UK posts a near 60% foreign ownership rate) but by sheer volume at almost $20 trillion in foreign investment. Foreign companies want to list in the U.S. to take advantage of higher valuations and foreign investors want to buy into U.S. markets despite those higher valuations.

The great thing about owning something everyone wants is that you can gatekeep it. Over the last decade, U.S. equity markets have increasingly become an instrument of national security policy. A Chinese company operating reusable launch vehicles, satellite constellations, and strategic space infrastructure would likely be viewed by the U.S. government through the lens of China’s Military-Civil Fusion strategy, which seeks to integrate civilian technological development with national defense objectives. It is noteworthy that the Chinese seem to have retired this term but certainly not the strategy. Under the regulatory framework established by Section 1237 of the National Defense Authorization Act and later evolved through Executive Orders 13959 and 14032, just such a Chinese space company would likely attract intense scrutiny from U.S. policymakers. Designation as a Chinese Military-Industrial Complex Company wouldn’t be automatic, but its role in a sector closely linked to Chinese military modernization would have made it a plausible candidate for restrictions on U.S. investment.

Even absent a sanctions designation, a Chinese SpaceX would have faced another hurdle: the Holding Foreign Companies Accountable Act (HFCAA), which requires U.S. regulators to inspect the audit work of foreign issuers and authorizes restrictions or delisting when those inspections cannot be performed. In 2022, the Public Company Accounting Oversight Board (PCAOB) finally gained inspection access to Chinese auditors, which temporarily removed immediate delisting risk for Chinese companies, but this access needs to be renewed yearly.

So a Chinese SpaceX would not have competed for capital on a level playing field with its American counterpart. While there may be no shortage of investors eager to plow funds into the Chinese space industry, by the early 2020s, the United States had begun to rethink a foundational assumption of globalization: that capital should flow freely regardless of geopolitical consequences. Increasingly, policymakers viewed American financial markets as a source of national power rather than merely a venue for price discovery.

Restricting access to U.S. markets became a way for the American government to deny strategic competitors the capital needed to develop advanced technologies, strengthen an industrial base, and ultimately challenge U.S. military and economic primacy.

The best in show

The most reliable equity trade of the past few decades has been U.S. technology. It is an extraordinary sector that has compounded and compounded and created the world’s most valuable companies. Despite analysts declaring (hoping, praying?) that the trade is finished every cycle, encouraging investors to rotate into emerging markets or Europe, the U.S. still proves unmatched at directing staggering amounts of capital at innovators and letting the survivors grow into giants — enriching investors and delivering surpluses to consumers and other corporations along the way. Anyone with access to a Nasdaq chart could tell you this.

Much less appreciated is how gated that trade is becoming. The U.S. government is tightening control over who gets to raise capital in America and under what terms. Hence the use of Section 1237, EOs 13959 and 14032, the HFCAA, CFIUS. It can be very expensive to be excluded from the deepest and most liquid markets in the world — we can expect that Washington will enforce very specific compliance from foreign investors and companies to grant entry, especially as the SEC launches a “Make IPOs Great Again” agenda.

America’s “exorbitant privilege” is the strength and ubiquity of the dollar. America’s equity privilege — the world’s persisting desire to own stakes in American firms and list on American exchanges — is no less powerful. SpaceX is a powerful demonstration of this equity privilege. Everyone wants dollars. Everyone wants to go to the moon. Everyone wants their portfolio to go to the moon. That’s the American dream, baby.

The article has two blind spots.

First, America’s equity privilege is not an independent source of power. It rests on the continued competitiveness of U.S. technology champions, their excess returns on capital, and their perceived growth runway. Once America’s relative technological competitiveness begins to decline, this so-called equity privilege becomes water without a source. Capital-market depth can amplify industrial and technological advantage, but it cannot substitute for it.

Second, China may not yet have a vertically integrated space champion like SpaceX, but its long-term potential in space is larger. One reason is China’s mixed state-private mechanism: state-owned and private players develop in parallel, creating a dual-engine model. By contrast, the U.S. government space ecosystem represented by NASA has clearly lost much of its old institutional strength.

Another reason is that China’s private space sector is using a wolf-pack strategy. More than a dozen companies are attacking different technical problems, competing fiercely, and iterating quickly. This is very similar to what happened in China’s auto industry. China did not produce one Tesla; it produced an entire swarm of highly competitive EV companies.

Chinese commercial-space companies also receive very high valuations in China’s own capital market. So the real question is not whether China lacks a SpaceX today. The deeper question is whether a decentralized, competitive, state-supported Chinese space ecosystem may eventually prove more powerful than America’s dependence on one mythologized super-company.