Winner-take-some (maybe)

The world is hedging stables vs. CBDCs

The stablecoin vs. central bank digital currency (CBDC) debate is usually framed something like this:

In one corner, the United States! Reigning champion of the regulated dollar-backed stablecoin. After President Trump prohibited federal agencies from establishing or promoting a CBDC, the U.S. has effectively halted work on a digital dollar — betting that private stablecoins can carry the banner of American monetary influence into the future.

In the other corner, China! Centralization nation! After Beijing slammed the door on private crypto, Chinese authorities have advanced a central bank digital currency (e-CNY) and wholesale platform (mBridge) — betting that sheer economic heft will provide China with options and internationalize the renminbi on Beijing’s terms.

The future method of cross-border payments is winner-take-all. The rest of the world sits in the stands, fretting about which pugilist to back. Bets are irrevocable! Dana White is on the South Lawn of the White House screaming, “Choooooose youuuur fighterrrrr and DEAL with the consequences!”

I mean. As much as I’d love to watch an AI-rendered video of two coins duking it out in what would be a manifestation of the ongoing financial cold war between two great powers… this framing does not reflect the reality of how the world is approaching next-generation payments.

While both the U.S. (mostly) and China have picked a path, most other countries are hedging their bets. And so long as each payment method has a viable route through retail and wholesale channels, there is a very probable future where stablecoins and CBDCs settle into some type of coexistence.

Hey neighbor, nice hedge!

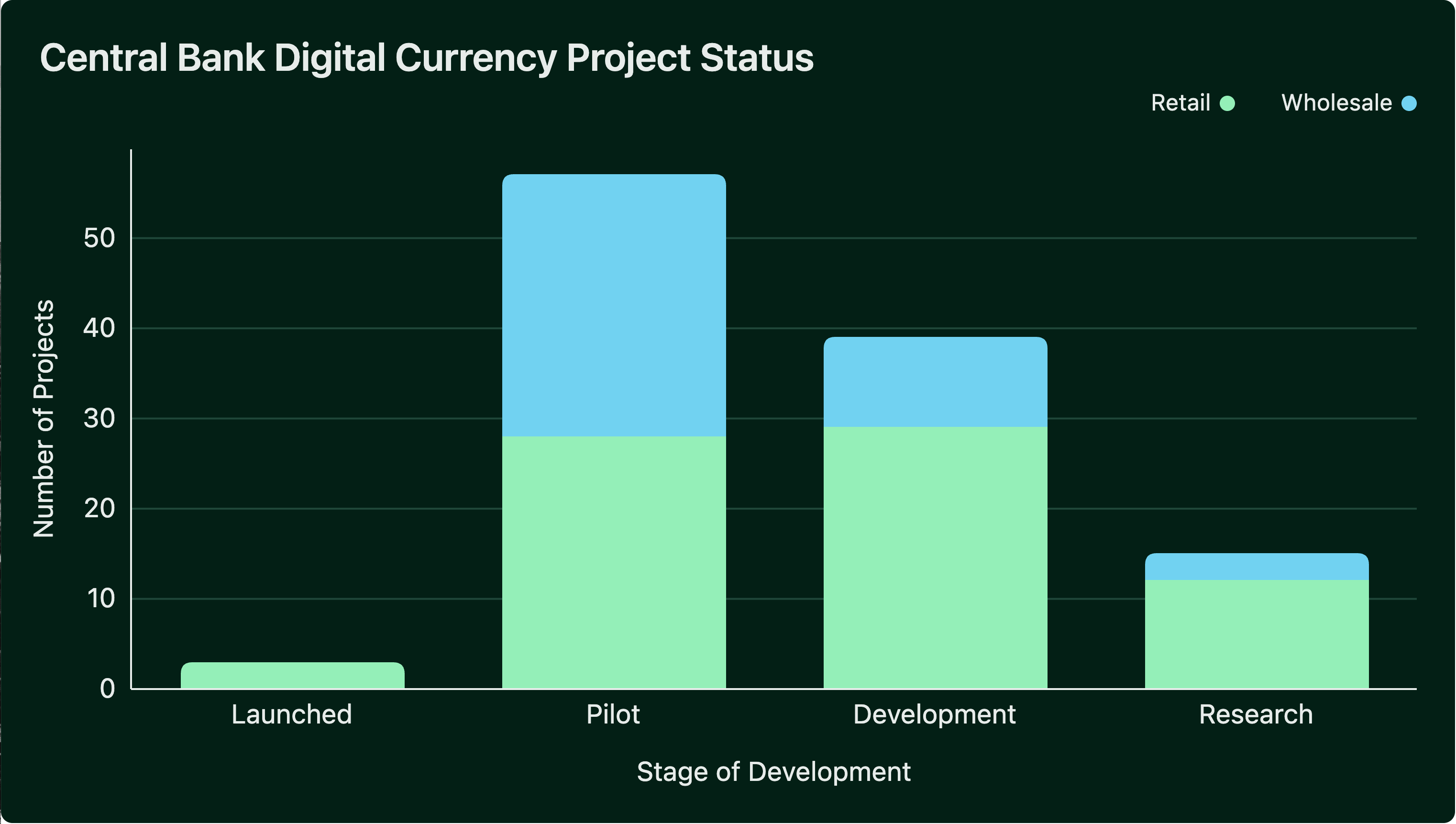

Last week, Fed Governor Waller suggested that CBDCs are a “solution in search of a problem” that most major central banks have abandoned. He also said that only the European Central Bank (ECB) and China remain serious about CBDCs. However, the data just doesn’t support him here.

The Atlantic Council’s CBDC tracker counts 146 countries and currency unions — over 98% of global GDP (including the U.S., more on that below) — still exploring central bank digital currencies. Now, many of these are experiments which do not necessarily equate to long-term commitment. But this isn’t just two central banks hammering CBDCs together on their lonesome.

Central banks are staffed by eminently sensible people weighing how to best protect their monetary sovereignty, lower payment costs, and avoid overdependence on either the U.S. or China.

Advanced economies continue to explore CBDCs and tokenized settlement systems while leaving breathing room for private non-dollar stablecoins, though none have yet achieved any significant scale. The ECB has made clear its preference for the digital euro, yet MiCA — the European Union’s landmark digital asset framework — takes a regulatory rather than prohibitive approach to stablecoins, leaving the door open.

Emerging markets, with the flexibility and hope of leapfrogging traditional finance, are leaning into both technologies. Brazil is developing a CBDC called Drex even as dollar stablecoins circulate widely in the country, while Kazakhstan has pursued both a digital tenge and a state-linked stablecoin, describing them as complementary rather than competing tools.

Layer cake

Looking at this debate as a binary between stablecoins or CBDCs loses rich context on how these instruments affect different payment layers and how they can coexist. Theoretically, a government could pursue:

Stablecoins and retail CBDCs for retail payments

Tokenized deposits for interbank transactions

Tokenized reserves for the final settlement in wholesale payments

While stablecoins appear to be dominating consumer payments, remittances, and parts of commercial settlement, most central banks and large multinational banks remain deeply interested in the wholesale layer where financial institutions move massive value across borders and states exercise their monetary authority.

China moved first here. mBridge — a shared ledger built by the central banks of China, Hong Kong, Thailand, and the UAE, and recently joined by Saudi Arabia and Macau — lets participating central banks issue their own currencies directly onto a common platform and settle cross-border payments between foreign banks in central bank money, without correspondents or reliance on SWIFT (i.e. without relying on the West).

The West, however, also has a wholesale contender: Project Agorá. Convened by the Bank for International Settlements and the Institute of International Finance, it brings together seven central banks — the Eurosystem, Japan, Korea, Mexico, Switzerland, the UK, Canada, and (notably) the Federal Reserve Bank of New York — along with more than forty major private financial institutions.

On the Agorá platform, tokenized commercial bank deposits handle the actual transactions, while final settlement occurs in tokenized central bank reserves. These feel very much like wholesale CBDCs, but I guess we’re going to call them tokenized central bank reserves. Unlike mBridge, which tries to cut out the traditional correspondent banking system, Agorá deliberately preserves it. It delivers the same atomic (simultaneous and irrevocable) settlement as mBridge, but keeps everything firmly inside the Western regulatory perimeter. Why aren’t more people talking about this?

Stablecoins probably won’t operate at the wholesale layer, so Agorá theoretically extends the dollar’s reach there and would (combined with tokenized deposits and reserves) round out the West’s options across payment layers. Right now, Agorá isn’t much more than a twinkle in its father’s eye. But the initial pilot proved successful. If deployed widely, it could keep the U.S. the dominant player across all settlement assets and types of payments, which, when combined with deep and liquid markets, makes a compelling system that other countries will be hard-pressed to opt out of.

Everybody hedges, sometimes

Global finance used to mean operating through a small handful of institutions and networks. Now the menu has expanded, shifting some of the decision-making power to those in the hedge. Hedging does come with trade-offs. Interoperability between systems is an open question, and hedging may lead to greater ecosystem fragmentation plus regulatory and compliance costs for financial institutions. The U.S. and China, as the two poles in this system, are most incentivized to pressure countries to pick a side. But whether either nation has the proper leverage remains an open question.

Most countries are choosing not to commit. A few countries have banned crypto and therefore likely won’t be using stablecoins. But maintaining more than one payment rail means that when any single system can be restricted through sanctions or other controls, redundancy protects financial access. Hedging is therefore likely to persist rather than resolve into a single winner. Countries will continue to run stablecoins, CBDCs, tokenized deposits, and wholesale platforms in parallel. We can take solace in the fact that the dollar remains central to this mix not because countries are required to use it, but because its liquidity and reach (now extended with Agorá) make it the most costly system to abandon.1

That you for proving another excellent overview of a topic that isn't receiving much attention. Your writing style is both informative and entertaining.

Perhaps our government officials and traditional media take umbrage with mBridge or suffer from an emerging form of Agorá-phobia, but then again, they don't seem to be terribly concerned about the exponential growth of our National Debt (funded and unfunded) nor do they seem to recognize the importance of our dollar remaining the world's primary global reserve currency. I also know a few congressional members who think CBDCs are oils that can relieve pain. That's why I recommend Hegemony to everyone I know who doesn't have their head firmly ensconced in the sand.

Keep up the great work, Ms. Hoversen.