Yuan-a pay in dollars?

How China domesticated the dollar

Despite a lot of hoopla about China’s nefarious master plan to dethrone the dollar, China still uses U.S. dollars. Lots of them.

The dollar is the world’s reserve currency and China, as the world’s second-largest economy, accumulates piles of dollars from trade and conducts a significant amount of its international commerce and finance in USD. So, perhaps reasonably, China wants to process dollars on its own terms. Over decades, China has assembled domestic and international options for dollar clearing and settlement — all of which have varying degrees of visibility to the American financial system.

This week we cover a quick snapshot of three rails, from most U.S.-connected to least, that allow China to process dollars. Note that we do not talk about China’s Cross-Border Payment System (CIPS) because it only processes RMB, not USD.

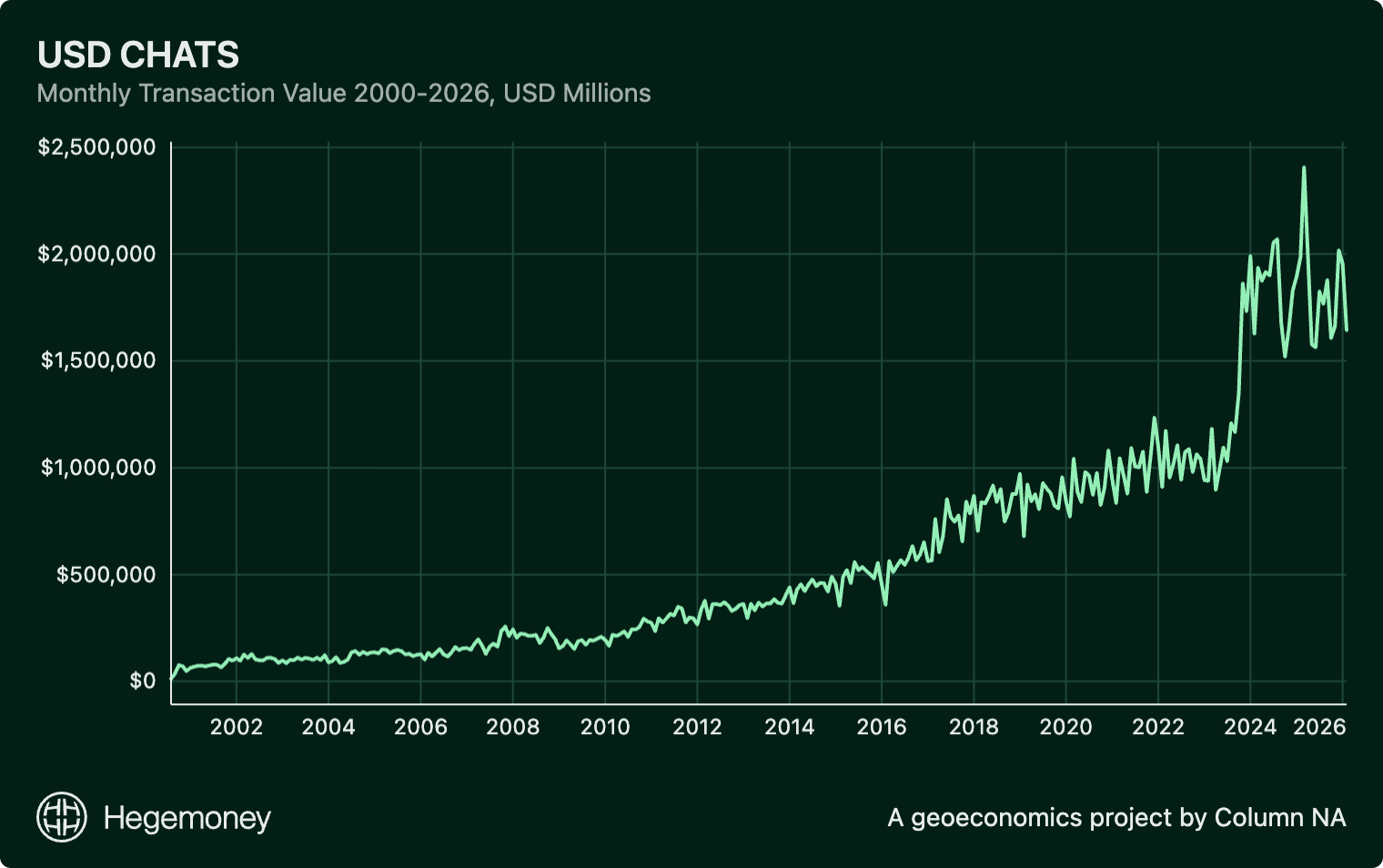

USD CHATS (Clearing House Automated Transfer System)

Let’s start with the most visible rail. USD CHATS is Hong Kong’s real-time gross settlement system (every payment settles individually and immediately) for U.S. dollar transactions. This system makes sure money actually moves when international banks (mostly licensed in Hong Kong) transact with each other in dollars. It was launched in 2000 to solve a practical problem: because Fedwire only operated during U.S. business hours, banks in Hong Kong settling transactions in dollars had to wait up to 12 hours for their transactions to settle in New York. This left them exposed to the risk that a counterparty could fail in that window (this is called Herstatt risk, after the 1974 collapse of a bank in Germany that had received Deutsche Marks but hadn’t yet delivered dollars in return, which wiped out a bunch of counterparties mid-settlement).

Banks participating in USD CHATS hold pre-funded dollar accounts at HSBC, and dollars are settled between banks locally and immediately during Asian business hours. The system handles not just interbank transfers but also stock market settlements, check clearing, and foreign exchange transactions across multiple currency pairs. Today it is one of the only large-value dollar payment systems in the world that operates outside the United States, with over 30 Chinese state-linked institutions now among its direct members and monthly transaction volumes exceeding $2 trillion. It is a major offshore valve for dollars.

The growth of USD CHATS reflects Hong Kong’s continuing role as China’s primary offshore dollar hub for trade payments, investment flows, hedging, and securities settlement — even as Beijing promotes the use of RMB elsewhere. In November 2023, Hong Kong Exchanges and Clearing launched a major tech upgrade that shortened the time between IPO pricing to trading from five days to two days and moved large volumes of IPO subscription money, refunds, and allotment payments from slow batch processing to direct real-time transfers through CHATS — causing the sharp jump in monthly transaction volumes in November 2023 and a permanently higher baseline afterward.

This rise in activity was likely driven by better tech. However, the broader policy context is worth noting. Just weeks earlier, at the October 2023 Central Finance Work Conference, Xi warned that “a small number of countries treat finance as tools for geopolitical games” and that financial sanctions “have presented new challenges to maintaining financial security.” Additionally, in December 2023, the United States expanded its secondary sanctions toolkit by issuing Executive Order 14114, which authorized penalties on foreign financial institutions facilitating transactions with Russia’s military-industrial base — a move widely seen as increasing pressure on third-country banks (including those in China) involved in sanctions evasion.

The timing of these events is likely coincidental, but they reflect a political environment in which Beijing has every incentive to deepen — not reduce — its capacity to process dollars outside American visibility. Talk about subtext!

Proprietary internal systems

Let’s take a beat to explain how the big four Chinese state-owned banks clear payments. For a long time, these banks cleared U.S. dollar transactions mainly through foreign correspondent banks. Eventually, these Chinese banks established U.S. branches as another option for dollar clearing. Bank of China went first in 1981 and then the rest followed starting in 2008. Establishing branches in the U.S. gave the Chinese banks a master account at the Federal Reserve and the ability to settle on Fedwire.

Given the global reach and sheer volume of transactions flowing through these banks, I wondered to what degree they tried to clear payments within the bank network using a book-to-book transfer (a payment that moves between two accounts at the same bank). I found that China Construction Bank (CCB) and Industrial and Commercial Bank of China (ICBC) have both built proprietary platforms to do exactly that. CCB developed its Global Multi-Currency Payment System (GMPS) which automatically routed each payment across two channels — book transfer or Fedwire. ICBC built a parallel system called FOVA, launched in 2006, which connects its domestic and overseas branches so they could process payments, remittances, and settlements on a single integrated platform. For GSIBs like ICBC and CCB, with their vast global branch networks and enormous transaction volumes, this internal book-to-book capability is a significant advantage. It allowed large volumes of USD payments to be settled entirely within the bank’s own ledger, often bypassing Fedwire and external correspondents altogether, which in fairness they still use.

An important note: There is no direct mention of GMPS or FOVA in either of these banks’ U.S. Resolution Plans (mandatory filings that every foreign bank with more than $50 billion in global assets must submit to the Federal Reserve). It’s possible these systems are no longer operational or have changed. But what we are trying to highlight here is China’s largest banks have publicly said they can and will process dollar payments book-to-book. I know that this is common for large banks with enormous pools of global liquidity. Many of those banks are our friends. It feels a lot different knowing that our greatest strategic adversary can use USD and avoid touching Fedwire or CHIPS entirely if it needs to.

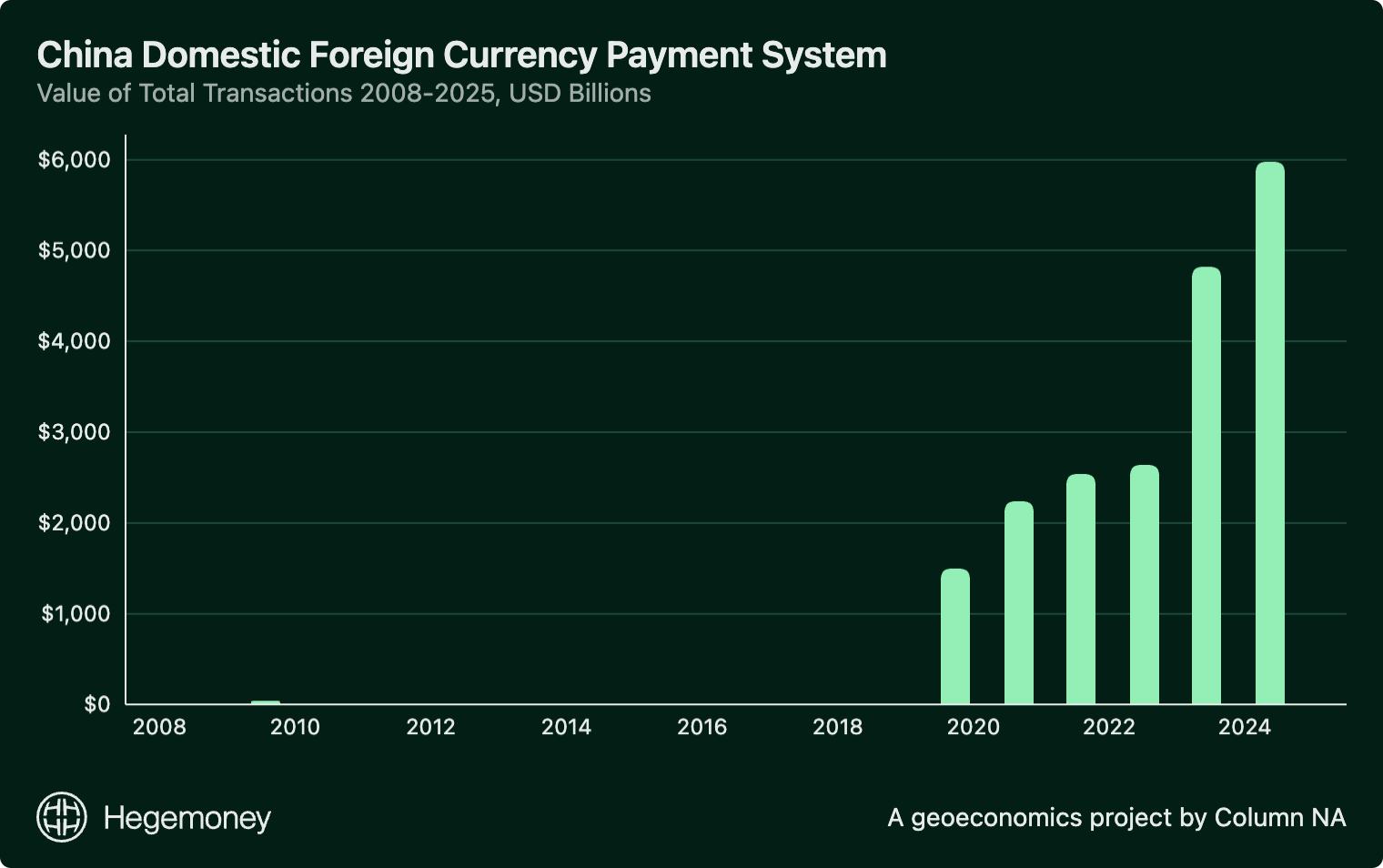

CDFCPS

This last rail is more obscure. The China Domestic Foreign Currency Payment System (CDFCPS) is a real-time gross settlement system developed by the People’s Bank of China and launched in April 2008. This onshore system clears and settles foreign-denominated transactions tied to domestic trades of goods and services (for example, an international company pays a domestic Chinese supplier in dollars). It can process payments in eight currencies: USD, HKD, GBP, EUR, JPY, CAD, CHF, and AUD — but data (albeit dated) suggest that USD dominates by a wide margin. Very little information is available on this system and it appears, judging from China’s Payment System Reports, that the name was changed to China Foreign Exchange Payment System (CFXPS) in the early 2020s.

Onshore volumes have surged in recent years alongside China’s expanding foreign trade, profit repatriation, outbound investment, and growing activity in FX derivatives and securities settlement. In Q2 2025, for example, this system processed 1.7 million transactions worth RMB 10.12 trillion (a daily average of 27,600 transactions or RMB 165.837 billion), a big increase from earlier periods.

Dedollarization is complicated

The RMB’s share of China’s cross-border payments has risen, and use of CIPS (China’s cross-border RMB payment system) has grown. But China’s absolute volume of dollar clearing continues to expand through diversified routes: highly visible offshore clearing in Hong Kong, more controlled onshore clearing via CFXPS, and nearly invisible internal bank ledgers.

Several of these systems developed in response to constraints in U.S. payments infrastructure, including Fedwire’s restricted operating hours or the slow processing speed of correspondent banks. The U.S. has started tackling these constraints with real-time payment initiatives like FedNow and RTP or discussion of expanded Fedwire operating days. Implementing and adopting these initiatives will become a matter of national interest. Inefficiencies in our payment systems invite the rest of the world to build workarounds that may increase demand for dollars, but exist outside America’s visibility and control — China has done exactly that and, in a sense, domesticated the dollar.1

Good one Jess

Indeed, we use lots of dollars. But to pass Hormuz, pay RMB. https://igreaterchina.substack.com/p/the-fiscal-architecture-of-chinese?utm_campaign=post-expanded-share&utm_medium=web