Patent pending

China's central bank amasses IP ammo for a fight over the future of money

Earlier this month, Nikkei published a story showing that Chinese entities made up 38 percent of total fintech patents over the last decade (2016–2025), with Chinese state-owned banks as top applicants and the drivers of technological development.

This isn’t a terribly surprising development for China watchers. The People’s Bank of China — its central bank — has published two national FinTech Development Plans: one covering 2019–2021 and the other 2022–2025. The most recent plan placed digital financial infrastructure firmly within China’s new infrastructure agenda, underscoring how, as Nik Milanović of This Week in FinTech states, Beijing “treats cashless payments as national policy.”

What may surprise even China watchers is that the People’s Bank of China (PBOC) has been filing patents through its Digital Currency Research Institute (DCRI) since its inception in 2016. And not just a couple, but hundreds of patents laying the foundations of digital yuan technology. This is unusual. Central banks do occasionally file patents — mostly on banknote security, though the Fed patented some check-clearing plumbing. However, none (outside of two Project Ubin filings from the Monetary Authority of Singapore) appear to have patented digital currency technology or operate at close to China’s scale. Which suggests Beijing could be preparing for a very… litigious… future of the financial system.

I call dibs!

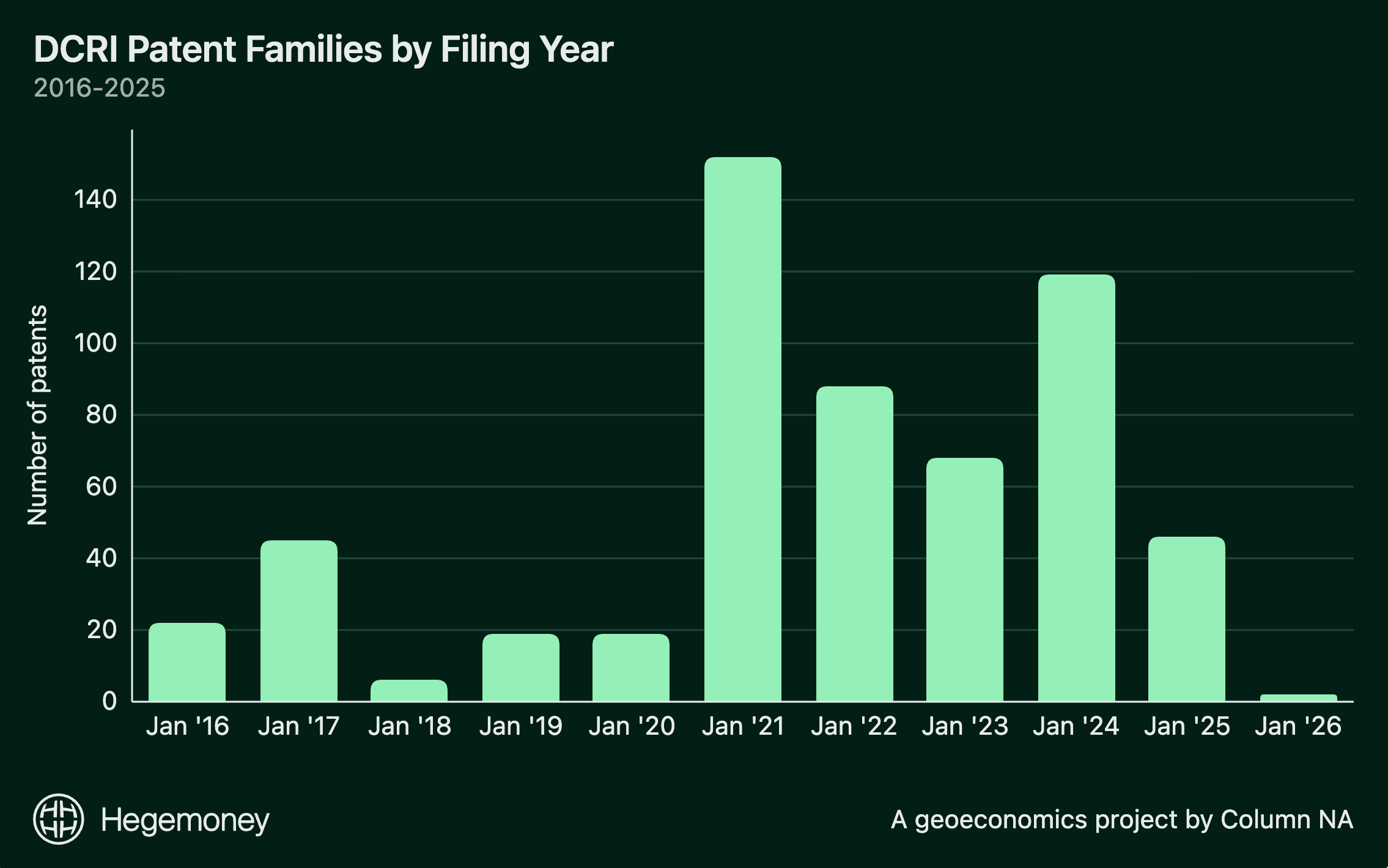

DCRI is a research team embedded within the central bank that functions as the primary research and development arm for China’s central bank digital currency (CBDC), the digital yuan, also known as the e-CNY. Based on our analysis of Lens.org data, the institute has filed approximately 586 patent families (see methodology note below). A patent family is one invention; protecting it in several countries requires a separate filing in each because a patent is only valid where granted. The institute began filing in 2016, but went into overdrive starting in 2021 — likely reflecting China’s shift from small-scale pilots into broader testing and cross-border experiments, such as mBridge.

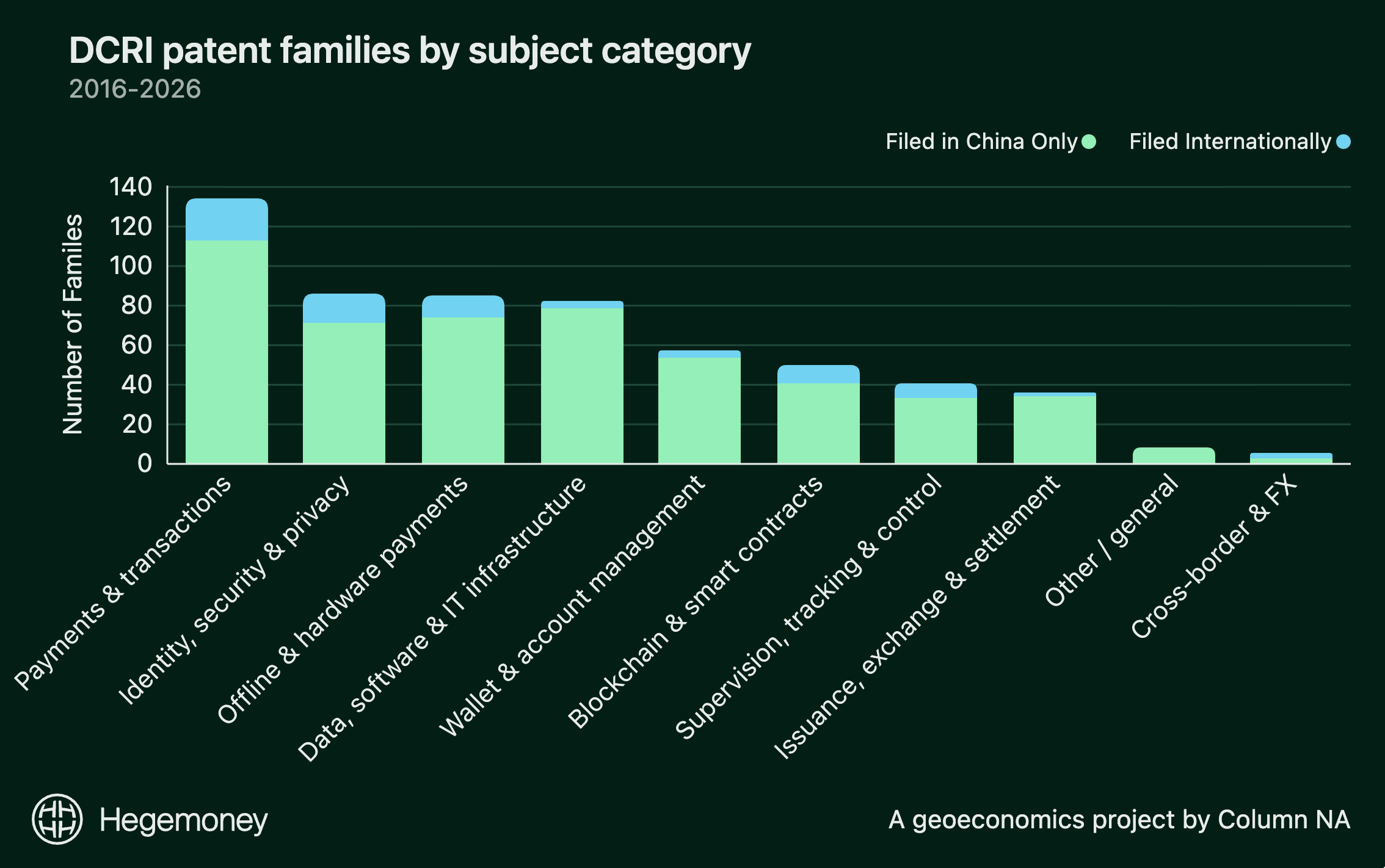

We have slotted DCRI’s filings into ten broad categories, which generally focus on the mechanics of operating a digital currency. Most of the 586 families (around 510) exist only in China. The rest were also filed internationally — chiefly in Europe, a little less often the United States, and never in America without Europe too.

Our analysis1 of The Lens data shows that major central banks like the European Central Bank, Bank of England, and Bank of Canada patent banknote security technology while the Fed’s filings cover legacy payment plumbing. The number of filings is not huge. The DCRI has filed more than all of these major banks combined.

So what is motivating China to claim 586 families of digital currency technology?

I might need that later

In China, domestic motivations usually come first. Bureaucracy is a powerful driver: the Chinese patent system strongly incentivizes volume through subsidies, rewards, and performance targets at multiple levels of government, driving explosive growth in Chinese patenting across firms, universities, research institutes, and individuals over the last couple decades. DCRI, as a state research institute under the PBOC, probably operates under this broader incentive environment. While many of its patents appear substantive and aligned with national priorities on digital yuan infrastructure, some portion of its hundreds of China-only filings could reflect the domestic incentives to file rather than the purely intrinsic value of each invention.

Beijing also likely viewed digital yuan-related patents as defensive against China’s private sector fintech giants. The digital yuan entered a payments market dominated by Alipay and WeChat Pay. A patent estate covering wallets, terminals, and settlement preserves the possibility of intellectual property rights over implementation methods should similar technologies become commercially significant.

Okay. But why file patents internationally for what is so far a largely domestic payments system? I’m not a patent lawyer (much to the chagrin of my father), but two motives come to mind:

First, export leverage. Chinese companies are already major global suppliers of payment hardware such as POS terminals, and the central bank’s research institute, looking ahead, has patented many of the methods that hardware would use if it carried digital currency. Some of those patent families are co-filed with the manufacturers themselves, including Huawei and the card maker Hengbao. If digital-currency payments spread abroad on Chinese hardware, foreign markets would likely be using methods the DCRI has already patented there. Rival equipment makers would face an unappealing menu: license from a foreign central bank (what does that even look like!?), engineer around the patents, or cede the market segment.

Second, beating your rivals to the punch. We have droned on about how countries are hedging their bets when it comes to a future financial system consisting of CBDCs or stablecoins. Well, China has committed to CBDCs, and patents make sure it has a claim while everyone else decides. Prior art — any evidence that an invention was already known before a rival’s filing date — has been used in the semiconductor industry, where firms disclosed research specifically to block competitors’ patents. A published patent application does the same thing. Once a patent application is published, it can be used to reject someone else’s similar patent later, even if the original application never gets approved.

I like to be prepared

But do these patents matter? A patent only works where it is granted, only if it survives challenge, and only against someone a court can practically reach. Still, the DCRI’s patent binge matters, for a few reasons:

First, patents turn what could have been a pure public good into state-owned intellectual property. A patent publishes the method but reserves the right to use it. Other central banks give both away — the BIS runs shared projects, the ECB posts its digital euro designs. China published hundreds of methods for implementing digital currencies while retaining ownership.

Second, the international filings suggest ambitions beyond hardware sales. Dozens of central banks are designing CBDCs, and many face engineering problems the DCRI has probably already patented solutions to. Granted patents could give China rights over parts of how rival systems work. Implementers would face a choice between licensing Chinese intellectual property, designing around it, or challenging it — a form of influence over the CBDC ecosystem we are only beginning to understand.

Third — and most important — China is complementing patents with its efforts to set international standards. Beijing has long treated technical standard-setting as a tool of industrial strategy and likely recognizes that patents become strategically valuable when they are incorporated into technical standards. Rysman and Simcoe found that patents attached to technical standards are cited about three times as often as comparable patents. DCRI’s patent clusters — smart contracts, digital identity, and wallet protocols — overlap substantially with the work programs of ISO/TC 307 and TC 68. Although the overlap is thematic for now — neither committee has published a single comprehensive CBDC technical standard — China is actively positioning itself in advance of fuller standardization.

I am on the lookout

Whether these patents ultimately become a source of influence will depend on three developments.

The outcome of DCRI’s international patent applications. If a substantial share of the European filings are granted — 52 are still pending — the portfolio becomes enforceable in one of the world’s largest markets, where the development of the digital euro is also advancing.

The incorporation of DCRI patents into future CBDC technical standards. Patents matter far more when they become part of the standards everyone else adopts.

The emulation of China’s strategy by others. If China’s approach becomes a model for other countries, patent ownership may become an increasingly important dimension of competition in CBDC technology — particularly if patented technologies become embedded in widely adopted systems.

Whether China’s patent spree ultimately translates into commercial or geopolitical influence remains uncertain. But it’s obvious China expects the infrastructure of money to be treated as strategic technology and the kind you’d better have your name on.

METHODOLOGY NOTE:

Patent data come from Lens.org, exported July 15–17, 2026. The universe is every record naming the PBOC’s Digital Currency Research Institute as applicant. The DCRI appears under four name strings — three English versions and 中国人民银行数字货币研究所 — and all four were queried, merged, and deduplicated. Three false positives were removed by hand, leaving 947 records: 657 applications, 243 grants, 47 search reports. The records collapse to 586 patent families, the counting unit used throughout. A few families show only international filings; in each case the underlying applications are Chinese, but the database groups bundled international filings separately from their domestic counterparts.

Counts reflect the database at export date; new publications move the totals. Chinese titles use the English family-member title where Lens has one; the remainder were translated by an LLM and flagged as such in the dataset. Translated titles are descriptive, not official.

Categories were assigned one per family by keyword rules applied to titles and abstracts, in fixed priority order with narrow categories matched before broad ones. Category counts are descriptive, not precise: families often span categories, and different rules would shift totals at the margin.